In a recent TV appearance, the author was briefly joined on air by a US professor full of the Manichean certitudes only a member of the transatlantic commentariat could possess in sharing his prescriptions about how best to ease the plight of Greece.

Declaring that it was ’about time that the ECB starting acting like a proper central bank’ he also insisted that the Greeks should quit the single currency, write down their debt by means of a devaluation, and so restore the country’s competitiveness at a stroke.

Now why didn’t anyone else think of that, professor!

The author’s first riposte—sadly unable to be fully developed in the course of the programme—was that the very reason so much of Europe is in the turmoil it is, and the reason the ECB is now so desperately trying to fend off any meaningful restructuring is that, absent a more centralist political structure, the Bank has long since abandoned its ’proper’ central banking function in order to become a quasi-fiscal, as well as a monetary agency—a fatal act of mission creep which has been made all the worse by the narrow parochialism of some of the national central banks operating under its umbrella.

As Irish critics of their governments’ (plural) shameful self-abasement make clear, the disaster engulfing their homeland was made much worse by decisions which were clearly aimed, not at solving the problem itself, but at sparing large banking creditors elsewhere in Europe from suffering the consequences of their own imprudence and greed—a stance apparently endorsed by Treasury Secretary Geithner’s veto of an IMF proposal to haircut Irish bank (not even sovereign!) bonds in November last year.

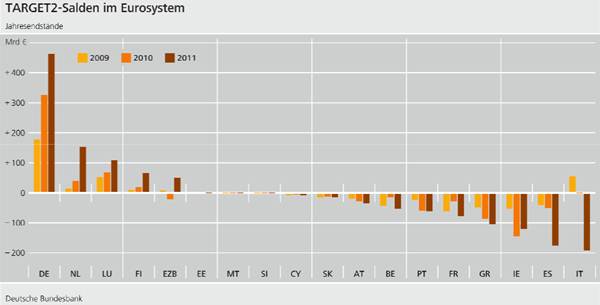

Instead, as Der Spiegel laid out in full this week, in its role as more than a ‘proper’ central bank (for which read: a Fed), the ECB has not only been active in directly supporting deadbeat governments across Europe’s periphery, but to help their compromised banks it bought almost €300 billion of the €380 billion in asset-backed securities issued last year; most of them purpose-built agglomerations of dubious worth and few of them subject to rigorous scrutiny by the national central banks who decide upon their eligibility for purchase.

The deeper issue is whether either the Greeks or their creditors would be better served by adding to the disruption of default and/or rescheduling the further perils of cutting adrift their remaining monetary anchor for, imperfect as it is, the euro at least spares them the fate of a 1997-8 Indonesia or a Thailand—or perhaps a Belarus of today.

As we have argued before, to resort to a currency change in order to make up for too high real wages, too low real returns on capital, and too mountainous a debt load is simply to succumb to money illusion—living standards will be reduced to reflect the harsh new reality, whatever happens at the borders.

Nor, strictly, would a Greece already stripped of access to private-sector credit have much to fear by way of properly-defined deflation, as long as arrangements are made to safeguard the supply of a medium of exchange during the transition to a lower-cost base, less state-bedevilled, more viable satellite nation.

In fact, by camouflaging the fall through re-denominating economic relations in a lower currency, we risk not just sweetening the pill, but neutralising its therapeutic effects altogether, as has so often been the case with the many serial devaluers and debasers across history.

Now it may be that, as my Greek friends insist, the very idea of a rational solution being reached is just so much wishful thinking in a land where, to quote the famous Tyke’s motto, people have been long used to being able to ‘eat all, sup all, pay nowt.’

My point is that, though no fan of the single currency as a macro-central banking construct, nor with the EU as a collectivist planning body, I don’t think the task is made any easier by dropping out of the euro.

Total or partial repudiation of foreign debt, a value-losing redenomination of local debt, and a significant decline in real incomes would happen either way. By dropping out of the Zone, however, the country might also become prey to an aggravating currency collapse (complete with offshore carpet-bagging). Even if that fate can be avoided – perhaps by the imposition of capital controls – the great likelihood is that it will quickly lapse into a supine maintenance of the politics of illusion, a path which could well induce such a rampant degree of inflation that it might culminate in the introduction of a further, new monetary unit explicitly linked to a harder, external alternative such as, irony of ironies, the euro!

When all else fails, do the right thing

Nor is there much appeal to be found in the alternative strategy of muddling along under the aegis of the euro, continually renegotiating rescue packages and privatisation auctions, in the hope that all will somehow come good. This is to deny both human nature and political reality.

For example, if the boss comes to you and says:-

’Sorry, Theo, but if we keep paying you €100 when we only get €80 of commercial value for your work, we will all be out of business by year end and none of us will earn anything at all. How about we all take a 20% pay cut now and work at re-orienting the firm and put in place a profit-sharing scheme so we can all benefit from our future success?’

That may be hard to take, but surely it is far superior to a managerial edict which states:

’Last year we made a €20 loss per person, so we are cutting all salaries by €5 now, €5 next year, €5 the year after and so on until first we balance the books and then discharge both our outstanding loans and the ones we will continue to have to contract in the interim. Only then, can anyone expect a move toward restoring existing pay-scales’

Not only are such partial adjustments ultimately a significant disincentive—both to employers and the employed—they leave a running sore on the body politic which must constantly be picked at, as each new budget brings another internecine squabble over which special interest group will bear the brunt and which will escape more lightly. As reform fatigue sets in, so will the scope for darker, more extreme political actors to make their mark as repudiationists or redistributionists.

No one wants to see the Weimar politics of ‘Fulfilment’ replayed across the fringes of Europe, however self-imposed this financial Versailles has been.

It is giving a hostage to fortune even to muse on this issue, but it might just be that—by force majeure, if for no other reason—the European political elite are slowly coming round to this realisation.

Le P’tit Caporal himself has begun to talk of private sector ’burden sharing’, while Merkel’s financial policy spokesman Meister has been forthright in declaring that ECB fears about the dangers of ‘restructuring; are ‘unfounded’ and Finance Minister Schaeuble has said that the region’s ‘woes’ cannot be solved without ‘private sector involvement’ – all code for a Danish-style bail-in.

The ECB, of course, cannot play honest broker here because its existential gamble that it could pass the costs of its little Dutch boy actions swiftly back to the member states has backfired badly, threatening it, barely a decade after its foundation, with the looming embarrassment of having to seek a recapitalisation and of suffering the loss of operational and doctrinal independence which might be the price exacted for such a gesture of state support.

In any case, what Herr Schaeuble should have said was that there could be no remedy without the involvement of the relevant private parties since, the ‘extend and pretend’ fudge under which we have been labouring for the past 3 1/2 years has already subjected many innocents in the ’Zone (as elsewhere) to all the needless collateral damage of interventionism, ranging from greater business uncertainty, to higher taxes, to raging commodity prices. As a result, the passing of the bill back to the ‘banksters’ directly responsible for the mess may finally have become the least politically unpalatable option—to which we can only offer up a loud, if tardy, ’Hurrah!’

Oh! And I’m sorry, but after more than three years of frantic and ineffective fire-fighting, it’s about time all you Mack Sennett Mainstreamers admitted the fact that we Austrians were right all along!

We told you from the outset that once a credit bubble bursts, ruthless accounting, a swift and honest acknowledgement of unavoidable contractual breach, and a speedy transfer of titles is the least—not the most—painful or protracted remedy available.

We further warned that to play the FDR card and call upon the already over-alienated resources of the Provider State in the vain attempt to avoid a bitter awakening from the reveries of the Boom would not only be to amplify the upheaval, but to make its resolution all the more intractable by moving it out of the realm of individual private action and their clearly-defined legal consequences into a Dystopia of disbursed responsibility, diffuse cost-sharing, and demagogic vote-buying.

You may well decry this as ‘shock therapy’, but it’s vastly more efficacious than your weaselly application of Chinese water torture!

The Bulge Bracket gets Bullish

The other topic of discussion on that same TV show was centred around the fact that one or two of the Bulge Bracket houses had called for commodities to trade much higher and, lo!, they miraculously moved up in price over the course of the next trading session or two!.

Only an unalloyed cynic could confuse this epiphany with the need to shore up Glencore’s post-IPO share price until all associated positions were neatly liquidated, but it was firstly a puzzle that this coincided with some of the same firms’ ’downgrading’ of China’s economic prospects and secondly laughable that a subsequent upward rotation in one or two EM stock indices was attributed to the renewed confidence in ’growth’ of which such marginally higher commodity prices was evidence, in flagrant denial of the fact that the monetary tightening which has been occasioning so much angst this spring has been undertaken in response to rising commodity prices!

Yet another fine example of ‘rational’ markets in action.

Are the bookies correct in their call? Only time will tell, but here you will find no enthusiasm for the hackneyed appeal to the long-term likelihood of actual physical shortages and resource peaks which the Street routinely makes the minute that its demand-based bullishness palls, by way this time of applying a sticking plaster to the punctures made in the last eight months’ hot-money inflation of asset and commodity prices.

So, rather than relying on the snake oil salesmen to tell us how we should think, let us go back to the basics for a moment to see if they will help clarify the situation in which we find ourselves today.

As we never cease to point out, the immediate effect of monetary injections is to reinvigorate business revenue streams and—at first—profits. And so it has been through the Great Reflation.

Thereafter, however, the monetary influx means prices begin to rise—stubbornly not in the sectors whose overbuilding and later collapse are the intended welfare recipients—and as their changes become more unpredictable, they both dilute the money’s growth-inducing potency and swamp out the signals conveyed by prices, signals upon which all economic decisions—whether taken by producers or consumers—must be based.

Unless the monetary authorities then abandon all sense of responsibility, their actions—however reluctantly taken—to counter this will tend to reduce real money supply, either actively (by slowing its nominal growth), or passively (by not adding sufficient to offset its declining purchasing power).

At this point, those whose continued expansion—and perhaps even their very continuance—in business has become too heavily dependent on the maintenance stimulus rush will again start to falter.

This last neatly describes conditions in many of the major economic zones of the world, with the current exception—thanks to the lunacy of QE-II—of the US.

Given that the Fed is about to withdraw from that policy (at least in the absence of enough weak economic data in the interim to shift the political balance back in the Permadoves’ favour), and given too, that just about everything that has happened in the asset markets since the beginning of that programme has moved in lock-step with its progressive implementation, this strongly suggests that even as the real world data begin to run less favourably, the financial world fantasy extrapolated has clearly been at hazard of being dispelled along with it.

Indeed, the lifting of this mirage of an eternal and largely indiscriminate bull-market is what remains the most likely candidate for the role of Gavrilo Princip in the setback which several markets suffered last month and not the operation of any more sinister forces as some have suggested.

So, the burning question now is whether commodity prices – and by extension those of shares and the riskier grades of credit – can shake off the disquiet caused by May’s sharp liquidation and validate the soundbite suppositions of the past few days.

With so much hot money still swilling around the world, readily available at low nominal and largely negative real rates of interest, we can never say never, but so many other beneficiaries of the Bernanke Bubble are either losing momentum and/or breaking trend, that it may be that the whole shell game has been busted pro tem.

Certainly, the fundamental backdrop is beginning to look less rosy, with Japan suffering a 13% decline in exports, Taiwan’s industrial expansion slowing, Thailand’s turning negative, US macro numbers registering a series of disappointments, UK businesses still cutting back on investment, and broad swathes of China’s corporate landscape experiencing a severe margin squeeze.

Our feeling is that for a significant rally to take place without enduring any further, intervening weakness (and regardless of the longer-term damage such actions would bring about), one of four things has to happen soon, listed here in a loose order of their assumed probability:-

- The Japanese government will forego the chance to introduce the meaningful, permanent fiscal rebalancing to which it might accustom the electorate under the guise of a supposedly temporary, disaster-relief measure and inveigle the BOJ into monetizing (albeit at one remove) the vast reconstruction effort needed in the country instead.

- The Chinese will prematurely relinquish their fight against the inflation which was unleashed by their huge, unfocused stimulus’ efforts of the past two years, in the estimation that the threat to the regime’s predominance posed by slow growth and falling employment is now greater than that posed by rapidly rising prices.

- As noted above, the Fed will find an excuse to revisit a programme of ’quantitative easing’ (i.e., money printing) without first being forced to sit by and watch a prolonged retrenchment in economic activity

- The US dollar will undergo a renewed, sharp decline, allowing existing carry-trades and ‘Risk On’ mixes to be reinstituted with the least demand for original thought. Here we should note that while, ceteris paribus, a flight from the dollar should not automatically boost commodity prices in other currencies, a combination of having a greater marginal impact in a much smaller market and the active contracting of paired trades does in practice tend to bring about such a broad appreciation.

If none of these detachments of the US Cavalry appears over the horizon in a timely enough fashion, or until there is unequivocal evidence that speculative appetite has somehow been reignited and – critically – refuelled in some other, wholly unforeseen fashion, our sense is that we have tougher times ahead, times that will provide less political cover and certainly a much reduced accounting leeway than the dominant school of macro-Micawberism has enjoyed for the bulk of these past two years of centrally-engineered rises in asset prices and the upwardly-sloped economic indicators which have accompanied them.

Great article & great site!

I think this interpretation of the ‘real money supply’ is right. Looking at the following chart of ‘Real money supply growth’ in the OECD, it seems that the latter statement has been in progress for some months now. (The chart is updated until March 2011):

http://greshams-law.com/wp-content/uploads/%27Real%27%20Broad%20Money%20Growth%20in%20the%20OECD.png