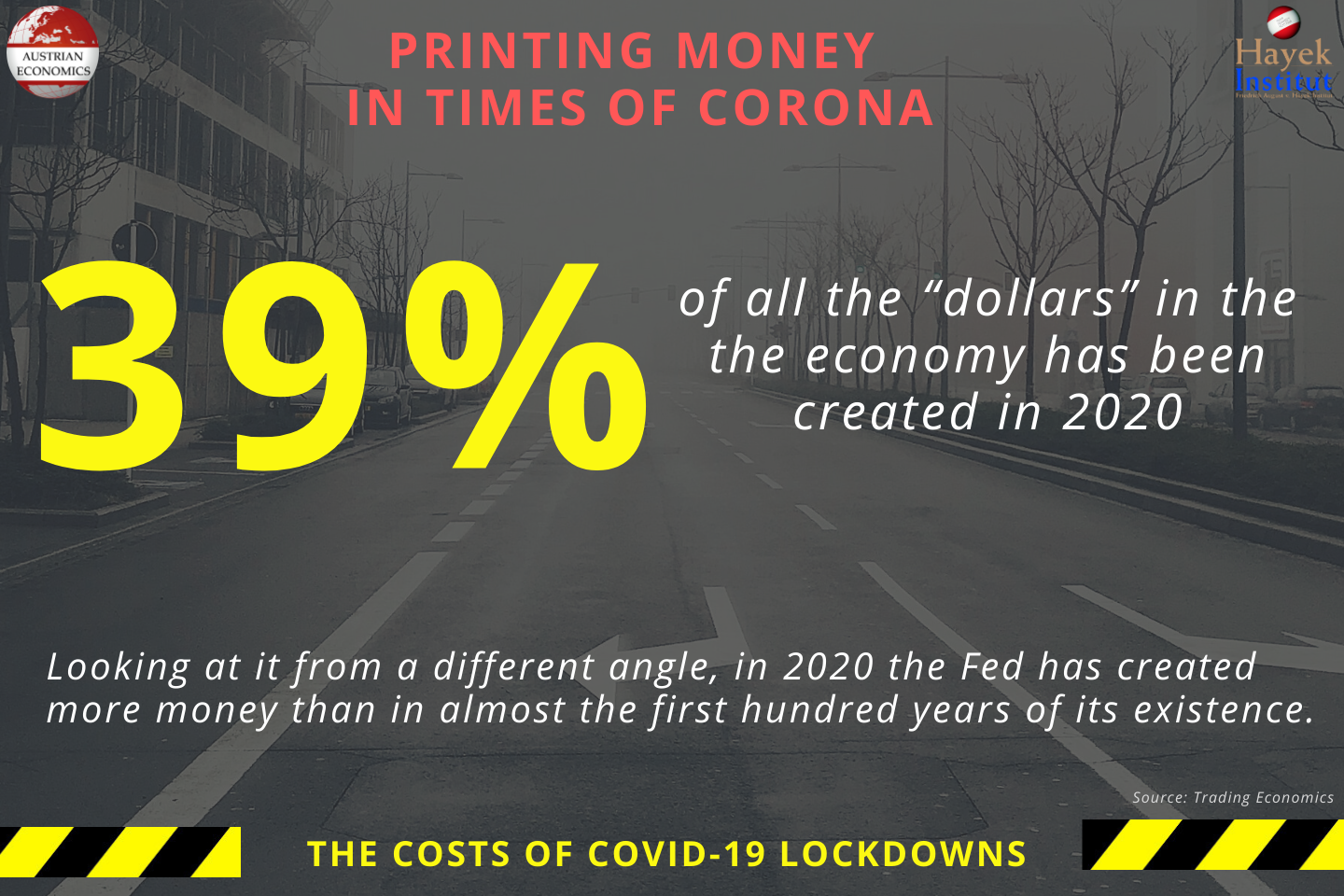

The world financial system is skating on thin ice, and that ice can crack at any moment.

The instabilities of the global paper money economy are evident everywhere. In Europe, the debt crisis is picking off one euro-member after another like the protagonists of a teenage horror movie, leaving us in no doubt what the final destination for the core is going to be. Yet – bizarrely and inexplicably – German Bundesanleihen still play the role of safe haven. In the U.S. of A., years of near-zero interest rates and two rounds of unprecedented “quantitative easing” have engineered a suspicious-looking rebound in equity markets and other financial assets, yet the victory of the interventionists over market forces looks hollow. Three years into the recovery, the economy is still sick. Manipulating financial markets seems one thing, generating prosperity quite another – only on Wall Street are the two the same. But according to the central bank’s chairman, if a policy fails it means you simply have to do more of it.

Only the intellectual and institutional inertia of the bloated financial industry, overfed on a rich forty-year diet of cheap money and ever-rising asset prices, is – for now at least – preventing a widespread rush for the exit. The industry is sitting on such a massive pile of inflated paper assets that there seem to be few alternatives to further feeding gluttonous governments and their clueless politicians. Additionally, things have gone from pretty bad to mind-blowingly worse too fast for most portfolio managers to comprehend – leading many to cling to the straws of time-worn investment routines and established asset allocation patterns. Did they not all learn back in money-manger school that government bonds were “safe assets”?

Smart ‘private money’ – nimbler, less consensus-oriented and, importantly, eager to sustain real spending power for the long run rather than beat some nominal index over the short run– is already running for the exit. Just look at the gold price and the prices of certain other real assets.

The tunnel vision of macroeconomics

My prediction is that things will get much worse very rapidly, and one of the reasons why I think this is inevitable is the inability of large sections of the political and financial establishment to even grasp what is going on. Of course, the reason for this is not any lack of intelligence. These are smart people. The reason is the oppressive dominance of an economic belief system that only provides a very narrow perspective on the full effects of an expanding supply of money.

And you want to know what really scares me? That the money-printer-in-chief, the man in charge of the printing press for the world’s dominant paper currency, the chairman of the U.S. Fed, not only shares this limited view of the effects of easy money, he is so completely beholden to the mainstream macro consensus that he is entirely incapable of even comprehending that his policy could do more harm than good.

Just look at this video of last week’s congressional hearings. The exchange between Congressman Ron Paul from Texas – the libertarian, Austrian-schooled Republican who is the only politician who ‘gets it’ – and the Fed chairman has been making the rounds on the web, and provoked already a lot of commentary. But what strikes me is not so much Bernanke’s struggle with explaining the monetary function of gold but something else. Something that indeed scares the living bejeesus out of me whenever I hear a Bernanke testimony.

Before I tell you what it is, let me stress that I don’t much like the widespread demonization of the Fed chairman. I have never met him but I cannot say that he comes across as an unpleasant individual. To the contrary, he seems to be a smart and decent person. Call me naïve, but I do not think that he is part of some conspiracy or any backroom dealing, or that he is in the pockets of the big Wall Street banks. I think he was sincere when he said that he never particularly cared about the management or the shareholders of the Wall Street firms he invariably bailed out and is still generously subsidizing with super-low funding rates and periodic debt monetization. He really believes that what he is doing is helping the U.S. economy and the U.S. people.

The problem is not that he is evil or dumb – I think he is neither – the problem is much bigger. Evil and dumb people can be dealt with. The deeply-convinced do-gooders in positions of almost unchecked power, those are the ones we should worry about, those who are full of good intentions but suffer from tunnel-vision, incurably in awe of their own theories and incapable of even beginning to grasp how what they are doing could make things worse. For keeping rates artificially low and bank reserves generously expanding is a form of constant market manipulation, and it is creating momentous dislocations and vast problems with as yet incalculable consequences – even if it does not presently generate instant hyperinflation or an intolerable expansion of the wider monetary aggregates, and thus looks deceptively harmless through Mr. Bernanke’s narrow prism of national account statistics.

Mr. Bernanke suffers from a blind side – there is an area of monetary phenomena, real and powerful phenomena, that are simply outside of his vision. It is the monetary blind side that all modern macroeconomists suffer from. For them two effects of an expanding money supply are visible, and only two:

1) The growth effect. Injecting more money lowers interest rates (temporarily) thus stimulates lending and borrowing, and leads to a (temporary) growth spurt. This effect is deemed unquestionably positive.

2) The inflation effect. More money means – all else being equal – that the purchasing power of the monetary unit drops. Prices tend to rise. Is this good or bad? Well, according to Bernanke and the mainstream consensus that he belongs to, the answer is, it depends. If there is a risk of that dreadful and debilitating deflation taking hold in the U.S. economy that seems to keep the chairman awake at night, then rising inflation is a good thing. But too much of it can be a bad thing.

So the two effects of the Fed’s money printing are higher growth and higher inflation. But here is the problem. This view is too narrow. It leaves out a very important, maybe the most important and potentially most damaging effect of money printing: the distortion of relative prices and the disruption of resource allocation and capital formation.

The Fed makes things worse

As I explain in detail in my upcoming book Paper Money Collapse – The Folly of Elastic Money and the Coming Monetary Breakdown, ‘elastic’ money is always destabilizing. Any expansion of the money supply (including bank reserves) must distort relative prices. Always and everywhere. Even if some fortuitous rise in money demand helps cushion the inflationary impact of expanding money and if inflation measures therefore remain contained. Even if the economy is weak and money printing is supposed to be a ‘stimulus’.

Specifically, every money injection must disrupt the market’s setting of interest rates and thus disorient the process of coordination between true savings and investment and capital formation.

Interest rates are market prices, and you interfere with them at your peril!

Continue reading at Paper Money Collapse

Comments are closed.