Much has been made in the press of the manipulation of LIBOR, without much explanation of the consequences for prices of all things that depend on supply and demand for bank credit. Outrage focuses on the activities of avaricious bankers, which is why the connection never gets made between relatively minor manipulations of credit pricing by banks and far larger manipulations by central banks.

It is the latter that should really concern us. Central banks persistently intervene in markets to keep interest rates below where they would otherwise be. This leads to artificially high prices for all assets, since they are bolstered by cheapened credit. The idea that we have a capitalist economy, where assets are priced on the basis of their productive value is untrue.

We are far removed from free markets, or prices that are fairly agreed between parties without state intervention. It is now impossible for any business to rely on market pricing, which is why there has been explosive growth in derivatives. Every derivative exists to hedge the risk in a transaction, and while that transaction is often another derivative, ultimately they all exist to hedge risk in real business activities. Some of this is sensible in free markets, such as a farmer selling his crop ahead of the harvest to maximise prices, or a mine selling its product forward in the knowledge it will have it to deliver; but the bulk of these derivatives only exist to hedge market uncertainties that are the consequence of government interventions.

According to the Bank for International Settlements, derivatives for non-financial customers world-wide totalled $46 trillion at the end of last year, 65% of world GDP, or about 100% ex-government. This is evidence that genuine entrepreneurial activity is being suffocated by interventions and manipulations, because an entrepreneur, by definition, is someone who exploits price differences, not one who seeks to hedge them.

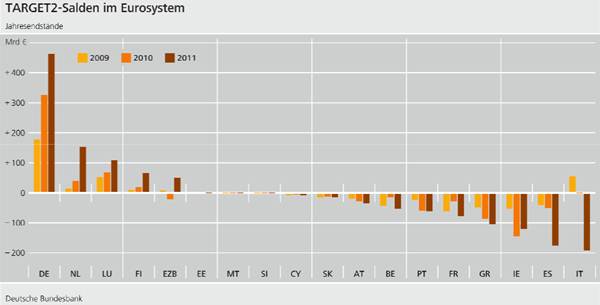

We should extend our condemnation of government intervention from interest rates to government-issued money itself. There can be no certainty in its future value, making it impossible for a businessman to calculate margins. An obvious example is the uncertainties facing any business involving the euro. No one knows who will be in the eurozone and who will be out of it next year, nor do they know if it will still exist, let alone whether the euro will be up or down. Uncertainties resulting from government interventions are economically damaging.

So all prices are no longer simply set by buyers and sellers but are manipulated by governments and central banks. The system that is failing is not capitalism, but price-rigging by governments. Governments will always try to persuade us that it is markets, and not them at fault. They have been doing this to varying degrees for a hundred years, ever since the abandonment of the gold standard. We are now on the last lap of this delusion.

We face the economic calculation problem identified by von Mises. It was the eventual undoing of the Soviet Union, and we have fallen into the same trap.

This article was previously published at GoldMoney.com.

There has always been government manipulation at the margin.

For example, right from 1694 the Bank of England issued more notes than it actually had gold.

But the key words in the above is “at the margin”.

The basic principle of honest banking and finance (yes there are such things) remained – i.e. that banks and so on take REAL SAVINGS and lend them out. Interest rates were influenced by government credit expansion (after all the basic point of creating a Central Bank is for government to be able to borrow money at cheaper interest rates than would otherwise be the case), but there still was a “market”, a distorted market but still a market.

In the United States also there were dreadful things – such as the mid 19th century National Banking Acts that made it illegal (yes ILLEGAL) for local banks to discount the paper of the big New York “national” banks.

And, of coruse, the creation of the Federal Reserve made matters far worse – just as the removal of all limits on the Bank of England (by the World Wars and by the 1931 “going off the gold standard” even the absurd rigged one of 1925 to 1931) tool banking and finance step-by-step away from a real market.

The so called “deregulation” of “Big Bang” (1986 and the orgy of legislation that came in the years after it – “deregulation” that really is thousands of pages of regulations)also took British banking and finance further and further away from a real market – from being lenders of REAL SAVINGS (rather than credit bubble game players).

However, it was still possible to talk of a “market” – real savings still mattered, the market was horribly distorted (like a human face in carnival mirror) but there was some sort of market.

But now?

Banking and finance is totally dependent on the credit money drip feed from the Central Banks.

Wall Street and City of London (and ….) are like junkies begging for yet another “fix”.

It is no wonder that the far left “Financial Times” newspaper (which blames all opposition to Comrade Barack Obama on his being “black” and people thinking he was “born outside the United States”) is still to be found in the City.

Why should not a far left newspaper (like the “FT”) not be popular among a gang of government welfare dependents like “the City”?