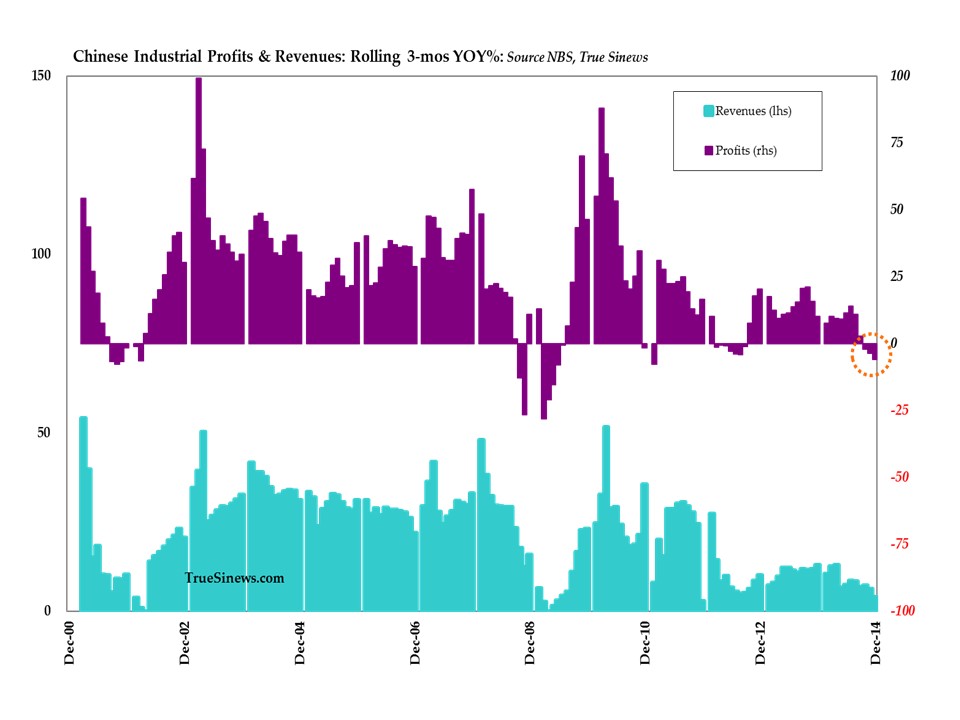

“I don’t think there is a problem that this will fix. I think it will just continue to compress yields into negative territory. If that’s the objective it will achieve it. The question is: will we regain European growth momentum and will labour markets pick up in particular outside Germany if we have a programme that buys debt including German sovereign debt ? So the bigger issue is for me a comparison with the US programme. The US QE programme was effective because a large part of the surge of US unemployment towards 10% was cyclical and the Fed provided a federal instrument – there is no risk-sharing because it was federal debt – and intervened in the most liquid market from which everything is priced.

“In Europe we don’t have such a bond market for, say, Eurobonds because the instrument doesn’t exist. It would be a risk-sharing instrument. Europe is not at that stage of political and fiscal integration. So whatever the ECB does they will not have a big impact on unemployment because most of European unemployment, unlike in the US, is not cyclical. European unemployment is high because of structural reasons. It is high because of inflexible labour market and product market structures, of pension systems, of medi-care systems, of a huge amount of government expenditure related to an ageing population. And so the better issue for Europe is to say: ‘we can help buy time as a central bank – governments should do the right thing’. And we’re seeing too little action too late from governments; in my view we’re seeing too much action too much upfront by the central bank and I think they should really work very hard for governments to face their responsibilities rather than taking on ever larger and ever more demanding responsibilities themselves.”

– Axel Weber, former president of the Deutsche Bundesbank, interviewed on Radio 4’s ‘Today’ programme, 22 January 2015, just prior to Mario Draghi’s announcement of a €1.1 trillion ECB money-printing programme.

“The guy with the asset price bubble question.. he is not coming back.”

– Tweet from Zero Hedge during the ECB press conference.

“When you look at Mr Wolf’s background … it becomes clearer why he supports these policies. He’s never mortgaged his house to open a small business. He lives in the fairy land of academics that believe printing paper will somehow be a signal to Directors (that have a fiduciary duty to act in the best interest of shareholders) to invest in expanding capacity?! ..that only the omnipotent power of the central planners can save the private sector by artificially holding down the major price signal in a ‘market’ economy.”

– ‘Manfred’, responding to Martin Wolf’s FT piece, ‘Draghi’s bold promise to do what it takes for as long as it takes’, 22 January 2015.

“YOU KNOW THE BULL MARKET IS LONG IN THE TOOTH WHEN

“When….. Start-ups are being started and IPO’s being raised to hunt Bigfoot… Nope… this is not a joke…And nope, this is not something you would see anywhere near market lows.

From today’s WSJ:

Start-ups are famous for setting big, hairy goals. Carmine “Tom” Biscardi wants to catch Sasquatch—and is planning an initial public offering to fund the hunt.

Mr. Biscardi and his partners hope to raise as much as $3 million by selling stock in Bigfoot Project Investments. They plan to spend the money making movies and selling DVDs, but are also budgeting $113,805 a year for expeditions to find the beast. Among the company’s goals, according to its filings with the Securities and Exchange Commission: “capture the creature known as Bigfoot.”

– Hat tip to Beijing Perspective. See also ‘Species of blue-green algae announces IPO’

Well, that was worth waiting for. Not. Future generations are unlikely to ask, ‘Where were you during the ECB’s announcement of QE, daddy ?’ Primarily because

a) Much of the detail of the stimulus was leaked the day beforehand, and

b) The real event of January was the Swiss National Bank’s capitulation in capping the franc’s peg to the euro.

Axel Weber’s assessment of the futility of euro zone QE is surely sufficiently articulate: a central bank is attempting to solve problems that can only be resolved through government action. A central bank by definition is limited in scope to the monetary sphere. What is required is tough love in the economic policy sphere – in France, in Greece, and elsewhere. Europe lacks the political and fiscal unity for Mario Draghi to do anything other than play games with the printing press and with a load of poor quality debt offering dubious yields. Central banks are not magicians, even if they behave like them.

And the ECB is coming late to the party in any case. In the words of Colin McLean, “the US and UK were dealing with a cyclical downturn, not deep-seated structural failure. In the euro zone, QE might further delay the need for structural reform..”

Financial historian Russell Napier last week discussed the Swiss National Bank’s surprise decision to abandon its own currency peg:

“The Swiss National Bank (SNB) failed to ‘fix’ the exchange rate between the Swiss Franc and the Euro. The simple lesson which investors must learn from this is – central bankers cannot fix very much. The inability of the Swiss National Bank to ‘fix’ the exchange rate will come to be seen as the end of the bull market in the omnipotence of central bankers.”

He went on to highlight some of the other things that investors erroneously believe central banks to have ‘fixed’:

“Central bank policy is creating liquidity.

Wrong – the growth in broad money is slowing across the world.

“Central bank policy is allowing a frictionless de-gearing.

Wrong – debt to GDP levels of almost every country in the world are rising.

“Central bank policy is creating inflation.

Wrong – inflation in most jurisdictions is now back to, or below, the levels recorded in late 2009.

“Central bank policy is fixing key exchange rates and securing growth.

Wrong – in numerous jurisdictions, from Poland to China and beyond, this exchange rate intervention is slowing the growth in liquidity and thus the growth in the economy.

“Central bank policy is keeping real interest rates low and stimulating demand.

Wrong – the decline in inflation from peak levels in 2011 means that real rates of interest are rising. The growth in demand in most jurisdictions remains very sluggish by historical standards.

“Central bank policy is driving up asset prices and creating a positive wealth impact which is bolstering consumption.

Wrong – savings rates have not declined materially.

“Central bank policy is creating greater financial stability.

Wrong – whatever positive impact central banks are having on bank capital etc. they have failed to prevent the biggest emerging market debt boom in history. That boom is particularly dangerous because either the borrower or lender is taking huge foreign exchange risks and because a large proportion of that debt has been provided by open-ended bond funds which can be subject to runs.”

The ongoing disaster that is the euro zone is tedious beyond words, so let’s change the subject. The Washington Post last week published a piece on Venezuela (different circus; same clowns) by Matt O’Brien. This is another cautionary tale of what happens to economies when bureaucrats insist on messing around with the price function. Having “defaulted on its people”, Venezuela may now be on the verge of defaulting on its debts.

“It shouldn’t be this way. Venezuela, after all, has the largest oil reserves in the world. It should be rich. But it isn’t, and it’s getting even poorer now, because of economic mismanagement on a world-historical scale. The problem is simple: Venezuela’s government thinks it can have an economy by just pretending it does. That it can print as much money as it wants without stoking inflation by just saying it won’t. And that it can end shortages just by kicking people out of line. It’s a triumph of magical thinking that’s not much of one when it turns grocery-shopping into a days-long ordeal that may or may not actually turn up things like food or toilet paper.

“This reality has been a long time coming. Venezuela, you see, has the most oil reserves, but not the most oil production. That’s, in part, because the Bolivarian regime, first under Chavez and now Maduro, has scared off foreign investment and bungled its state-owned oil company so much that production has fallen 25 percent since it took power in 1999. Even worse, oil exports have fallen by half. Why? Well, a lot of Venezuela’s crude stays home, where it’s subsidized to the you-can’t-afford-not-to-fill-up price of 1.5 U.S. cents per gallon. (Yes, really). Some of it gets sent to friendly governments, like Cuba’s,in return for medical care. And another chunk goes to China as payment in kind for the$45 billion it’s borrowed from them.

“That doesn’t leave enough oil money to pay bills. Again, the Bolivarian regime is to blame. The trouble is that while it has tried to help the poor, which is commendable, it has also spent much more than it can afford, which is not. Indeed, Venezuela’s government is running a 14 percent of gross domestic product deficit right now, a fiscal hole so big that there’s only one way to fill it: the printing press. But that just traded one economic problem — too little money — for the opposite one. After all, paying people with newly printed money only makes that money lose value, and prices go parabolic. It’s no wonder then that Venezuela’s inflation rate is officially 64 percent, is really something like 179 percent, and could get up to 1,000 percent, according to Bank of America, if Venezuela doesn’t change its byzantine currency controls.

“Venezuela’s government, in other words, is playing whac-a-mole with economic reality. And its exchange-rate system is the hammer. It goes something like this. The Maduro regime wants to throttle the private sector but spend money like it hasn’t. Then it wants to print what it needs, but keep prices the same like it hasn’t. And finally, it wants to keep its stores stocked, but, going back to step one, keep the private sector in check like it hasn’t. This is where its currency system comes in. The government, you see, has set up a three-tiered exchange rate to try to control everything — prices, profits, and production — in the economy. The idea, if you want to call it that, is that it can keep prices low by pretending its currency is really stronger than it is. And then it can decide who gets to make money, and how much, by doling out dollars to importers at this artificially low rate, provided they charge what the government says.

“This might sound complicated, but it really isn’t. Venezuela’s government wants to wish away the inflation it’s created, so it tells stores what prices they’re allowed to sell at. These bureaucrat-approved prices, however, are too low to be profitable, which is why the government has to give companies subsidies to make them worthwhile. Now when these price controls work, the result is shortages, and when they don’t, it’s even worse ones. Think about it like this: Companies that don’t get cheap dollars at the official exchange rate would lose money selling at the official prices, so they leave their stores empty. But the ones that are lucky, or connected, enough to get cheap dollars might prefer to sell them for a quick, and maybe bigger profit, in the black currency marketthan to use them for what they’re supposed to. So, as I’ve put it before, it’s not profitable for the unsubsidized companies to stock their shelves, and not profitable enough for the subsidized ones to do so, either..

“.But just like Venezuela has defaulted on its most basic obligations to its people — like, say, laundry detergent — it might also default on its financial ones. It can’t afford anything, not food, not diapers, and not bond payments, if oil stays around $50 a barrel. Now, investors have assumed that they’d be able to seize Citgo, which is owned by Venezuela’s state-owned oil company, as payment if the country ever defaulted on its debt. But now it looks like that’s not true. That, together with falling oil prices, is why credit default swaps, basically debt insurance, on Venezuela’s 5-year bonds haveexploded the past few months. The fiscal situation is so dire that Citgo, which, remember, supposedly wouldn’t count as a part of the Venezuelan state, is planning on taking out $2.5 billion in debt to give to its parent company, which would presumably pass it along to the government. This makes sense, as much as anything does in Venezuela, because Citgo has a higher credit rating than the government, so it canborrow, and if it defaults, it will just be as if the country sold it.

“It’s a man-made tragedy, and the men who made it won’t fix it. Maduro, for his part, blames the shortages on the “parasitic” private sector, while the food minister doesn’t get what the big deal is since he has to wait in line at soccer games.

“So it turns out Lenin wasn’t just right that the best way to destroy the capitalist system is to debauch the currency. It’s also the best way, as Venezuela can tell you, to destroy the socialist one.”

At last week’s press conference to announce the ECB’s first iteration of QE (if history is any guide, there will be more), Mario Draghi claimed to see no evidence of inflation whatsoever. Perhaps Mario Draghi lets someone else manage his property, stock and bond portfolio.

I was beginning to fade when I read that Central Banks do not cause inflation…..that is until I read the last paragraph.

These people are now so confused by their own gobledigook they now truly believe that inflation has to do solely with rising retail prices.

Or,do they?

Perhaps, just perhaps we are witnessing the next collapse in socialism. There is a long history of this. And in ‘The West’ socialism writ large is Central Banking/financial regulationism. Maybe, these people didn’t realise that the collapse of the Soviet Union in 1991 was just the end of the pervious act and the next act was them.

Whatever, it’s not going to end well, but I am not sure for whom.