“Donald Trump looks like the villain in a movie where the hero is a dog.”

– The internet.

Which four letter word still has an amazing capacity to cause offence, anxiety and aggravation ? In the world of investment, that word would have to be

R-I-S-K.

Do we even have a workable definition of what it means ?

Author Guy Fraser-Sampson, in ‘The Pillars of Finance’, points out that before the Second World War, financial thinkers had a somewhat humbler perspective on the subject:

“..while before the War there was eager discussion as to what risk might be, and whether it was the same thing as uncertainty, there was total agreement that whatever it was it was probably too complex an animal ever to be fully understood and, in particular, that it was incapable of mathematical calculation.” [Emphasis ours.]

The American academic Frank Knight published ‘Risk, Uncertainty and Profit’ in 1921. As he wrote, some forms of uncertainty are measurable. There is, for example, empirical observation with regard to the occurrence of a number of discrete outcomes, such as the rolling of dice.

Then there is ‘true uncertainty’, such as the chances of a house in a particular area catching fire in any given year. The probability of dice throws is capable of mathematical calculation – albeit the outcome is still not guaranteed – whereas the chance of a house burning down is not. In relation to fire insurance, we can only use statistical inferences drawn from prior observation.

“The import of this distinction.. is that the first.. type of probability is practically never met with in business, while the second is extremely common. It is difficult to think of a business ‘hazard’ with regard to which it is any degree possible to calculate in advance the proportion of distribution among the different possible outcomes. This must be dealt with, if at all, by tabulating the results of experience. The ‘if at all’ is an important reservation.”

Ludwig von Mises published ‘Human Action’ in 1949 and ‘The ultimate foundation of economic science’ in 1962. That adjective ‘human’ says a lot. As Mises would point out, human values are variable, subjective, often indefinable. Since market outcomes are the result of human decision-making based on these values, past outcomes cannot predict the future.

Guy Fraser-Sampson:

“You can only employ the techniques of the natural sciences such as physics if you can use things like empirical observation extrapolated from scientific experiments, and apply mathematical techniques to analyse the data. Yet financial data is the result not of physical phenomena but of human action, which is in turn caused by human decision making, which is sequentially prompted largely by emotion. So finance is behavioural, not physical. It is at best a social science studying human behaviour, like psychology or sociology, and can never be a physical science.. It is for this reason that neither observation nor mathematical techniques can ever offer any valid universal guide to future outcomes.”

And then Harry Markowitz came along. In a 1952 article (‘Portfolio Selection’ in Journal of Finance 7 (1)), Markowitz, a 25-year-old mathematician with no experience of investment whatever, argued that a diversified portfolio must always be preferable to an undiversified one. Variance of return, in his words, was undesirable. Markowitz did not explicitly state that risk and volatility (variance) were the same thing. But he might as well have done. As a result of the article, volatility and risk became synonymous and, in the words of Peter L. Bernstein,

“Markowitz had put a number on investment risk.. [After Markowitz] risk and variance have become synonymous.”

So-called modern portfolio theory – which is neither modern, nor a theory, in any recognisably scientific sense – holds that the investment risk of any asset is the same as, or can be expressed as, the variance of its historical returns (volatility). As Fraser-Sampson points out, a belief that risk and calculated volatility are the same thing rests on a number of assumptions, among them:

• That risk is capable of mathematical calculation;

• That variance of return is a valid risk proxy;

• That periodic return is a valid measure of performance;

• That normal distribution applies to investment returns over time;

• That the past is a good guide to the future;

• That we may safely ignore the time value of money.

It also requires the belief

• That all investors are rational;

• That all investors have access to the same information at the same time, and

• That all markets are perfect.

The UK financial regulator, the FCA, has just issued a report claiming that roughly six in 10 customers of wealth managers and private banks are receiving “unsuitable” advice and that 23% of customer files it assessed showed a “high risk” of the client having received irrelevant advice. Problems identified included “investment allocations being made that did not accord with the customer’s expectations and / or match the customer’s attitude to risk.”

We wonder whether the regulator has a definition of risk. If it does, we wonder whether it matches that of Harry Markowitz.

We offer our own definition of risk. It has comparatively little to do with day-to-day price volatility. It has everything to do with the risk of ruin, of permanent loss. Or as Carl Richards nicely defined it,

“Risk is what’s left over when you think you’ve thought of everything.”

In the FCA’s document Finalised Guidance FG15/1: Retail investment advice the UK regulator, under ‘Assessing risk’, offers the following counsel:

“3.55: The findings suggested many firms did not understand how the tools they use work, including what they are (and are not) designed to do. Firms should use a tool only where they are satisfied that it provides outputs that are appropriate and fit for purpose. Firms need to recognise where a tool has limitations and mitigate these.”

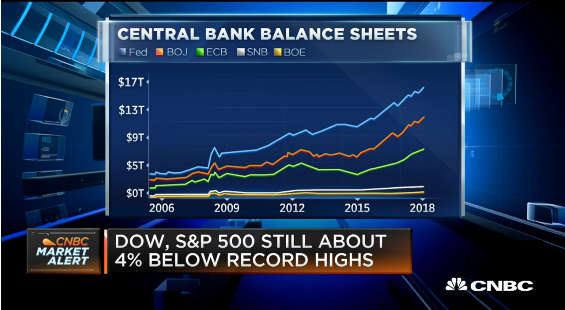

This counsel was aimed at investment managers. It was not, apparently, aimed at the Bank of England (or the Federal Reserve, or the ECB).

Now imagine for a second that the paragraph in question actually was aimed at central banks, and among the tools in question were QE. And ZIRP. And NIRP.

“..many [central banks] did not understand how the tools they use work, including what they are (and are not) designed to do.”

“[Central banks] should use a tool only where they are satisfied that it provides outputs that are appropriate and fit for purpose.”

“[Central banks] need to recognise where a tool has limitations and mitigate these..”

In its weekend markets report, the Financial Times included this seemingly innocuous review:

“[2 year] German and Japanese yields were down 2bp at minus 0.35% and steady at minus 0.02% respectively”.

We are already through the looking glass. Bond investors are already sipping tea with the Mad Hatter, locking in guaranteed losses lending to insolvent governments.

And financial markets are now braced for a monetary policy tightening by the Federal Reserve. Judging by Friday’s price action, not all investors are cheered by this prospect.

What, if anything, is the solution ?

Following the Markowitz / Modern Portfolio Theory playbook, the investment industry has long favoured something akin to the “60/40” approach: put c. 60% of your client assets into (indexed) equity markets, and put c. 40% into (indexed) bond markets.

60/40 is designed to be a “diversified” portfolio.

But what if the combined onslaught of acronyms GFC, TARP, QE, ZIRP and NIRP has transformed the investment landscape ? Turned it, almost literally, upside down ? What if unprecedented monetary stimulus has so dangerously distorted prices and yields that a) cash has become functionally irrelevant as an asset class, b) most bonds are now the polar opposite of a safe haven, and c) most equity markets are objectively overvalued and at risk of a perhaps major reversal ?

What if stock and bond markets, far from being assumed to be uncorrelated, were both, at some point perhaps quite soon, to enter a prolonged bear market ?

In that environment, 60/40 gets obliterated. With the full approval of the regulator.

Investing through the looking glass requires a fundamental reappraisal of modern portfolio theory.

The ‘bonds as safe assets’ assumption needs to be entirely discarded.

Indexed equity investing and passive equity investing need to be viewed with extreme caution. (Buying ‘cheap’ market exposure at what may be near to the top of the market is likely to be penny wise and pound foolish.)

Investors probably need greater asset diversification than they have ever previously considered.

We believe that there only two sustainable ways of harvesting attractive returns from the financial markets over the longer term. One of them is from exploiting straightforward price momentum, hence our preference for systematic trend-following as portfolio insurance. Alongside gold.

The other is from classic ‘value’ investing. That is, purchasing the shares of businesses run by principled, shareholder-friendly management when those shares are trading at a discount to any objective assessment of their fair value or versus the rest of the market. The ‘discount’ factor offers a ‘margin of safety’ that is simply not present in the credit market or in most western equity markets.

But from a valuation perspective, both that ‘margin of safety’, and classic Ben Graham-style ‘net net’ investments, we believe, can be found in certain pockets of the international stock markets. Where are we looking ? Japan is a stand-out, for one.

There are simply more inexpensive stocks in the Japanese market than anywhere else: the absolute number of stocks valued at less than 10 times earnings in Japan, for example, is greater than across the markets of China, the US and the UK combined. And the managers with whom we invest in Japan also report that the change in corporate behaviour as a by-product of Abenomics (with an enhanced focus on shareholder value, returns to shareholders, dividend payments and share buybacks) is real.

Amid an environment of broken markets and shattered hopes, we see huge attractions in returning to solid, time-honoured fundamentals.

Good article.

I have always been amazed that whole academic schools get blinded by new theories without taking the trouble to identify the underlying assumptions.

This is just the tip of this iceburg.

Fascinating