Source: http://davidstockmanscontracorner.com/the-war-on-savers-and-the-200-rulers-of-world-finance/

There has been an economic coup d’état in America and most of the world. We are now ruled by about 200 unelected central bankers, monetary apparatchiks and their minions and megaphones on Wall Street and other financial centers.

Unlike Senator Joseph McCarthy, I actually do have a list of their names. They need to be exposed, denounced, ridiculed, rebuked and removed.

The first 30 includes Janet Yellen, William Dudley, the other governors of the Fed and its senior staff. The next 10 includes Jan Hatzius, chief economist of Goldman Sachs, and his counterparts at the other major Wall Street banking houses.

Then there is the dreadful Draghi and the 25-member governing council of the ECB and still more senior staff. Ditto for the BOJ, BOE, Bank of Canada, Reserve Bank of Australia and even the People’s Printing Press of China. Also, throw in Christine Lagarde and the principals of the IMF and some scribblers at think tanks like Brookings. The names are all on Google!

Have you ever heard of Lael Brainard? She’s one of them at the Fed and very typical. That is, she’s never held an honest capitalist job in her life; she’s been a policy apparatchik at the Treasury, Brookings and the Fed ever since moving out of her college dorm room.

Now she’s doing her bit to prosecute the war on savers. She wants to keep them lashed to the zero bound—-that is, in penury and humiliation—–because of the madness happening to the Red Ponzi in China. Its potential repercussions, apparently, don’t sit so well with her:

Brainard expressed concern that stresses in emerging markets including China and slow growth in developed economies could spill over to the U.S.

“This translates into weaker exports, business investment, and manufacturing in the United States, slower progress on hitting the inflation target, and financial tightening through the exchange rate and rising risk spreads on financial assets,” she said, according to the Journal, which said she made the comments on Monday.

In the name of a crude Keynesian economic model that is an insult to even the slow-witted, Brainard and her ilk are conducting a rogue regime of financial repression, manipulation and unspeakable injustice that will destroy both political democracy and capitalist prosperity as we have known it. They are driving the economic lot of the planet into a black hole of deflation, mal-distribution and financial entropy.

The evil of it is vivified by an old man standing at any one of Starbucks’ 24,000 barista counters on any given morning. He can afford one cappuccino. He pays for it with the entire daily return from his savings account where he prudently stores his wealth.

After a working lifetime of thrift and frugality his certificates of deposit now total $250,000. Yes, the interest at 30 bps on a quarter million dollar nest egg buys a daily double shot of espresso and cup of milk foam.

What kind of crank economics contends that brutally punishing two of the great, historically-proven economic virtues——-thrift and prudence—-is the key to economic growth and true wealth creation?

In this age of relentless consumption and 140 character tweets, what kind of insult to common sense argues that human nature is prone to save too much, defer gratification too long, shop too sparingly and consume too little?

Forget all of their mathematical economics and DSGE model regressions. Our 200 unelected rulers are enthrall to a dogma of debt that is so primitive that it’s just plain dumb.

By purchasing existing debt with digital credit conjured from the “send” key on central bank computers, they make room for more and more of it. And they do so without the inconvenience of deferred consumption or an upward climb of interest rates owing to an imbalance of borrowings versus savings.

Likewise, by pegging the money market rate at zero or negative, they enable even more debt creation via daisy chains of re-hypothecation. That is, the hocking of any and all financial assets that trade at virtually zero cost of carry in order to buy more of the same and then to hock more of them, still.

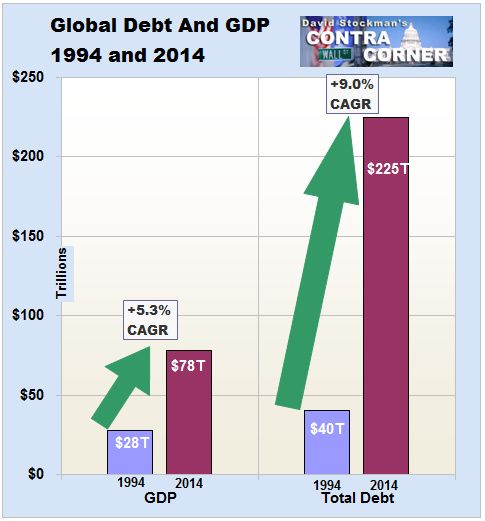

The truth is, the world is up to its eyeballs in debt. Since the mid-1990s, the 200 rulers have ignited a veritable tsunami of credit expansion. Worldwide public and private debt combined is up from $40 trillion to $225 trillion or 5.5X; it has grown four times more than global GDP.

Whatever has caused the growth curve of the global economy to bend toward the flat-line, it surely is not the want of cheap debt. Likewise, the recurring financial crises of this century didn’t betray an outbreak of unprecedented human greed; they were rooted in heretofore unimagined excesses of leveraged speculation.

That’s what margined CDS wraps on the supersenior tranches of portfolios of CDOs squared were all about. That’s how it happened that upwards of 10% of disposable personal income in 2007 consisted of MEW ((mortgage equity withdrawal). It’s also how the US shale patch flushed $200 billion of junk debt down drill boreholes that required $50 per barrel oil to breakeven on the return trip.

Likewise, you don’t need any fancy econometrics to read the next chart, either. Since 1994 US debt outstanding is up by $45 trillion compared to a $11 trillion gain in GDP. If debt were the elixir, why has real final sales growth averaged just 1.0% per annum since Q4 2007—–a level barely one-third of the peak-to-peak rates of growth historically?

If the $10 trillion of US debt growth since the eve of the Great Recession was not enough to trigger “escape velocity”, just exactly how much more would have done the job?

Our 200 financial rulers have no answer to these questions for an absolutely obvious reason. To wit, they are monetary carpenters armed with only a hammer. Their continued rule depends upon pounding more and more debt into the economy because that’s all a central bank can do; it can only monetize existing financial claims and falsify the price of financial assets by driving interest rates to the zero bound or now, outrageously, through it.

But debt is done. We are long past the peak of it. After 84 months of ZIRP, Ms. Brainard’s call for “watchful waiting” at 25bps is downright sadistic.

Where does she, Janet and the rest of their posse get the right to confiscate the wealth of savers in their tens of millions? From the Humphrey-Hawkins Act and its dual mandate?

Puleese! It’s a content-free enabling act etched on rubber bands; it memorializes Congress’ fond hope that the people enjoy an environment of price stability, fulsome employment and kindness to pets.

This elastic language hasn’t changed since 1978, meaning that it mandates nothing. In fact, it enabled both Paul Volcker’s 21% prime rate and Yellen’s 84 months of free money to the Wall Street casino———-with nary a legal quibble either way.

So what is at loose on the land is not public servants carrying out the law; its a posse of Keynesian ideologues carrying out a vendetta against savers. And they are doing so on the preposterous paint-by-the-numbers theory that when people save too much we get too little GDP, and when we don’t have enough GDP, we have too few jobs.

That’s essentially rubbish. Jobs are a function of the price and supply of labor and the real level of business output, not the amount of nominal expenditure or GDP. And most certainly not that arbitrarily measured GDP clustered inside the USA’s open borders, criss-crossed as they are by monumental flows of global trade, capital and finance.

Likewise, “savings” fund the investment component of GDP today and the growth and productivity capacity of tomorrow, not a hoarder’s knapsack of bullion.

Besides, the claim that a nation experiencing 10,000 baby boom retirements per day has too little savings is not only ludicrous; its empirically wrong.

Household savings at the recession bottom in 2009 amounted to $670 billion according to the GDP accounts. In 2014 it was nearly $50 billion or 7% lower.

During that same five year “recovery” period, consumption expenditures for owner occupied housing rose by $150 billion or 12%, and personal spending for new autos increased by $400 billion or 58%.

So “savers” didn’t get in the way of spenders, nor do these figures prove that ZIRP had anything to do with it anyway.

The $1.35 trillion spending for owner-occupied rent shown below, for example, is not a real number in the first place. Its an “imputed” estimate pulled out of BEA’s nostrils based on a half-assed survey which asks a few thousand homeowners what they would rent their castle for if they were in the landlord business.

They don’t have a clue, of course. Nor does the 7.5% of GDP accounted for in this manner actually exist anywhere in the known universe outside of the BEA’s charts of accounts and the Keynesian DSGE models which simulate them.

And the same is true for personal savings. It’s a measure of nothing real on main street—– in part because 60% of US households have zero liquid savings beyond rounding error amounts. Actually, the “personal savings” account might better be designated as the Errors and Omissions account.

That’s because the above “savings” figures are a statistical residual that falls out when the $18 trillion +/- of spending side accounts are stacked up next to a nearly equivalent pile of income side accounts. As Jeff Snider documented the other day, the numbers in both stacks are revised so much that this 3.5% crack in the GDP wall amounts to little more than noise.

Likewise, ZIRP didn’t have much to do with the fact that auto lenders—especially the legions of subprime nonbank operations that have sprung up with junk bond financing——have been extending credit to anyone who can fog a rear view mirror.

Indeed, since mid-2010 when the auto recovery incepted, auto credit outstanding is up by $350 billion or by nearly 90% of the $400 billion gain in auto sales.

Needless to say, virtually 100% debt financing of an auto sales boom is no more sustainable than was the MEW financing of household consumption last time around. Like then, the pool of credit worthy borrowers has been depleted, meaning that it is only a matter if time before the debt fueled auto boom of recent years goes pear-shaped.

Even then, what will bring on this calamity is the inexorable collapse of the used car prices, not an end to the Fed’s “watchful waiting” on the money market rate.

At present upwards of 80% of all new car sales are either leased or loan financed. But the economics of leasing depend heavily on the “residual” or resale value of the vehicle; and loan financing late in the sales recovery cycle depends on the ability of the marginal buyer to generate enough trade-in value to qualify for a new loan–—-even at today’s 120% LTV ratios.

And that’s where the skunk in the woodpile is hiding. During the next 5 years a veritable tsunami of used vehicles will come off lease and loan and flood the used car market, thereby reversing the virtuous cycle of debt fueled new car sales that may well have peaked last fall.

Thus, in 2009 nearly 2.5 million vehicles came off lease, but by 2012 that number was down to 1.56 million owing to the 2007-2009 auto sales collapse. By contrast, an estimated 3.1 million vehicles will come of lease in 2016, 3.4 million in 2017 and upwards of 15 million in the next four years.

In short, ZIRP didn’t trigger the auto debtathon, even as it punished savers for 7 years running. What happened, instead, is that the Wall Street junk financed boom in auto lending fueled a run-up in used car prices, thereby temporarily goosing the loan/lease residuals upon which an increasing share of US households rent their rides between visits of the repo man.

Indeed, banging the interest rate lever hard on the zero bound for so long has now taken our 200 financial rulers into truly Orwellian precincts. In the quote reproduced above, and echoed by B-Dud, Goldman’s plenipotentiary at the New York Fed, it is claimed that “tightening credits spreads” are a reason to keep the policy rate unchanged. That is, the market is doing the Fed’s job voluntarily and preemptively!

No it isn’t. Credit spreads have been wantonly and dangerously compressed by massive central bank intrusion in the financial markets. Yet now that they are twitching with the ethers of normality, the monetary politburo takes that as a sign to keep their boot on the savers’ neck.

But shown below is the lunatic extent of their misfeasance in real time. From a cold start in 2015, the assembled central banks of the world have driven nearly $6 trillion of sovereign debt into the nether world of negative yields, and with each passing day it gets more absurd.

Now well-rated corporate debt like that of Nestle is passing through the zero bound and practically all of Japan’s 10-year or under maturities are there.

These fools think this is owing to such nonsense as Brainard’s blather about “stresses in emerging markets including China” and that “slow growth in developed economies could spill over to the U.S…….(translating) into weaker exports, business investment, and manufacturing in the United States, slower progress on hitting the inflation target……etc.”

The implication, of course, is that stalling world growth requires more central bank stimulus, and even a scramble toward NIRP by central banks which have not yet joined the Looney Tunes brigade of the ECB, Sweden, Denmark, Switzerland and Japan.

Not even close. The amount of debt pouring into the negative yield basket is owing to speculators buying bonds on NIRP enabled repo. Their cost of carry is nothing, and the prices of NIRP bonds keep on rising.

So yields are plunging into the financial netherworld because speculators are front-running the financial death wish of the central banks.

Until they stop. Then look out below. The mother of all bubbles—-that of the $100 billion global bond market—-will blow sky high.

At length, savers will get their relief and our 200 financial rulers will be lucky to merely end up in the stockades at a monetary version of the Hague.

Meanwhile, the War On Savers continues to transfer hundreds of billions from savers to the casino in the US alone—–even as the global economy careens towards a deflationary collapse.