There is almost complete unanimity among economists and various commentators that inflation is about general increases in the prices of goods and services. From this it is established that anything that contributes to price increases sets in motion inflation.

A fall in unemployment or a rise in economic activity is seen as a potential inflationary trigger. Some other triggers, such as rises in commodity prices or workers’ wages, are also regarded as potential threats.

If inflation is just a general rise in prices as the popular thinking has it, then why is it regarded as bad news? What kind of damage does it do?

Mainstream economists maintain that inflation causes speculative buying, which generates waste. Inflation, it is maintained, also erodes the real incomes of pensioners and low-income earners and causes a misallocation of resources. Inflation, it is argued, also undermines real economic growth.

Why should a general rise in prices hurt some groups of people and not others? Or how does inflation lead to the misallocation of resources? Why should a general rise in prices weaken real economic growth?

Also, if inflation is triggered by various factors such as unemployment or economic activity then surely it is just a symptom and therefore doesn’t cause anything as such.

To ascertain what inflation is all about we have to establish its definition. Now to establish the definition of inflation we have to establish how this phenomenon emerged. We have to trace it back to its historical origin.

The essence of inflation

Historically inflation originated when a country’s ruler such as king would force his citizens to give him all their gold coins under the pretext that a new gold coin was going to replace the old one. In the process the king would falsify the content of the gold coins by mixing it with some other metal and return diluted gold coins to the citizens. On this Rothbard wrote,

More characteristically, the mint melted and re – coined all the coins of the realm, giving the subjects back the same number of “pounds” or “marks”, but of a lighter weight. The leftover ounces of gold or silver were pocketed by the King and used to pay his expenses.[1]

On account of the dilution of the gold coins, the ruler could now mint a greater amount of coins and pocket for his own use the extra coins minted. (He could now divert real resources to himself). What was now passing as a pure gold coin was in fact a diluted gold coin.

The increase in the number of coins brought about by the dilution of gold coins is what inflation is all about. As a result of the increase in the amount of coins that masquerade as pure gold coins, prices in terms of coins now go up (more coins are being exchanged for a given amount of goods).

Note that what we have here is an inflation of coins i.e. an expansion of coins. As a result of inflation, the ruler can engage in an exchange of nothing for something (he can engage in an act of diverting resources from citizens to himself).

Also note that the increase in prices in terms of coins comes on account of the coin inflation. Observe however that it is the increase in coins brought about by the dilution of gold coins that enables the diversion of resources here to the ruler and not an increase in prices as such.

Under the gold standard, the technique of abusing the medium of the exchange became much more advanced through the issuance of paper money un-backed by gold.

Inflation therefore means an increase in the amount of receipts for gold on account of receipts that are not backed by gold yet masquerade as the true representatives of money proper, gold.

The holder of un-backed receipts can now engage in an exchange of nothing for something. As a result of the increase in the amount of receipts (inflation of receipts) we now also have a general increase in prices.

Observe that the increase in prices develops here on account of the increase in paper receipts that are not backed up by gold.

Also, what we have here is a situation where the issuers of the un-backed paper receipts divert real goods to themselves without making any contribution to the production of goods.

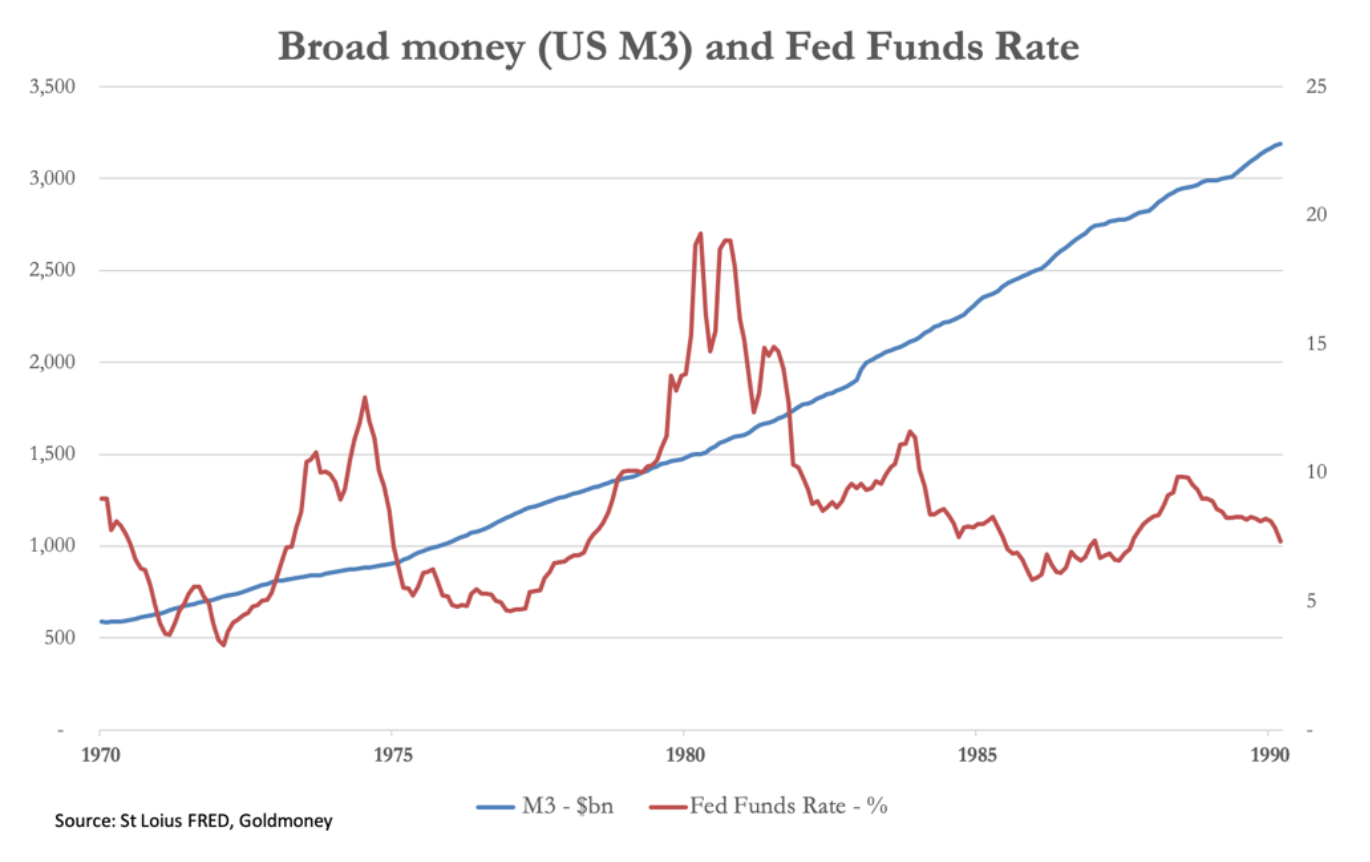

In the modern world money proper is no longer gold but rather paper money; hence inflation in this case is an increase in the stock of paper money.

Observe that we don’t say that the increase in the money supply causes inflation. What we are saying is that inflation is the increase in the money supply.

Inflation – increases in money supply – and wealth destruction

Note that increases in the money supply set in motion an exchange of nothing for something. They divert real funding away from wealth generators towards the holders of the newly created money. This is what sets in motion the misallocation of resources, not price rises as such.

Real incomes of wealth generators fall, not because of general rises in prices, but because of increases in the money supply. When money is expanded i.e. created out of “thin air”, the holders of the newly created money can divert goods to themselves without making any contribution to the production of goods.

As a result wealth generators who have contributed to the production of goods discover that the purchasing power of their money has fallen since there are now less goods left in the pool – they cannot fully exercise their claims over final goods since these goods are not there.

Once wealth generators have less real resources at their disposal this is obviously going to hurt the formation of real wealth. As a result real economic growth is going to come under pressure.

General increases in prices, which follow increases in money supply, only point to an erosion of real wealth. Price increases by themselves however do not cause this erosion.

Can increases in commodity prices cause inflation?

According to most economists an important factor behind a general increases in prices is increases in commodity prices.

We have seen that inflation is brought about by a deliberate act of currency debasement – on a gold standard by issuing un-backed by gold paper money, whilst on a paper standard an increase in the supply of paper money.

An increase in commodity prices as such is not related to an act of embezzlement. For instance, in a true market economy an increase in the price of oil versus the prices of other goods is just a reflection of changes in people’s demand. Obviously it has nothing to do with an act of currency debasement brought about by the increase in money supply out of “thin air”.

Also, if the price of oil goes up and if people continue to use the same amount of oil as before, people will be forced to allocate more money to oil. If people’s money stock remains unchanged, less money is available for other goods and services.

This of course implies that the average price of other goods and services must come down. Again, remember a price is the sum of money paid for a unit of a good. (The term “average” is used here in conceptual form. We are well aware that such an average cannot be computed).

Note that the overall money spent on goods doesn’t change; only the composition of spending has altered, with more on oil and less on other goods. The average price of goods or money per unit of good remains unchanged.

Hence, the rate of increase in the prices of goods and services in general is going to be constrained by the rate of growth of money supply, all other things being equal, and not by the rate of growth of the price of oil.

It is not possible for increases in the price of oil to set in motion a general increase in the prices of goods and services without the corresponding support from money supply out of “thin air”.

We can then conclude that the so-called general increase in prices that seems to follow an increase in a commodity price such as oil, is in fact on account of an increase in the money supply out of “thin air”. (Note that since an injection of money doesn’t enter all the markets instantly, a general increase in prices ensues on account of previous increases in money supply).

Most economists, when discussing the issue of general increases in prices, which they label inflation, never mention the word money. The reason for that is the lack of a good statistical correlation between changes in money and changes in various price indexes such as the CPI.

We hold that whether changes in money supply cause changes in prices cannot be established by means of statistical correlation.

We suggest that a statistical correlation or a lack of it, between two variables shouldn’t be the determining factor in establishing causality. One must figure it out by means of reasoning as to the structure of causality.

Can inflation expectations trigger a general price rise?

We have seen that as a rule a general increase in the prices of goods emerges on account of an increase in the amount of money paid for goods, all other things being equal.

The key then for general increases in prices, which is labeled by popular thinking as inflation, is increases in the money supply.

But what about the situation when increases in commodity prices ignite inflation expectations, which in turn strengthens a general increase in prices? Surely then inflation expectations must be also an important driving factor behind the general increase in prices?

According to most economists’ inflation expectations are the key driving factor behind increases in general prices.

Once people start to anticipate higher inflation in the future they raise their demands for goods at present thus bidding the prices of goods higher.

Also, according to popular thinking, workers expectations for higher inflation prompt them to demand higher wages. Increases in wages in turn lift the cost of producing goods and services and force businesses to pass these increases on to consumers by raising prices.

It is true that businesses set prices and it is also true that businessmen while setting prices take into account various costs of production. However, businesses are ultimately at the mercy of the consumer who is the final arbiter.

The consumer determines whether the price set is “right”, so to speak. Now, if the money stock did not increase then consumers wouldn’t have more money to support the general increase in prices of goods and services, all other things being equal.

Hence, on account of expectations for higher prices in the future, all other things being equal, consumers will not be able to raise their demand for goods at present and bid the prices of goods higher without having more money. Consequently, the amount of money spent per unit of goods will stay unchanged.

So irrespective of what people’s expectations are, if the money supply hasn’t increased then peoples’ monetary expenditure on goods cannot increase either. This means that no general strengthening in price increases can take place without an increase in the pace of monetary pumping.

Note that inflationary expectations as such don’t cause a currency debasement, so in this sense an increase in so-called inflation expectations has nothing to do with inflation – i.e. an increase in money out of “thin air”.

Imagine that somehow the Fed did manage to convince people that central bank policies are aimed at stopping inflation and maintaining price stability, yet at the same time the central bank also raises the rate of growth of money supply.

Even if inflationary expectations were stable the destructive process will be set in motion regardless of these expectations on account of the increase in the rate of growth of money. Note that people’s expectations and perceptions cannot offset this destructive process.

It is not possible to alter the facts of reality by means of expectations. The damage that was done cannot be undone by means of expectations and perceptions.

Conclusion

Contrary to the popular definition inflation is not about general rises in prices but about increases in money out of “thin air”. Inflation is an act of embezzlement.

On a gold standard inflation is about the increase in un-backed by gold money. On a paper standard inflation is about an increase in the supply of paper money. The general increase in prices as a rule develops on account of the increase in money.

The harm that most people attribute to rises in prices is in fact due to increases in money supply out of “thin air”. Policies that are aimed at fighting inflation without identifying what it is all about only make things much worse.

When inflation is seen as a general increase in prices, then anything that contributes to price increases is called inflationary. It is no longer the central bank and fractional-reserve banking that are the sources of inflation, but rather various other causes.

In this framework, not only does the central bank have nothing to do with inflation, but, on the contrary, the bank is regarded as an inflation fighter.

On this Mises wrote,

To avoid being blamed for the nefarious consequences of inflation, the government and its henchmen resort to a semantic trick. They try to change the meaning of the terms. They call “inflation” the inevitable consequence of inflation, namely, the rise in prices. They are anxious to relegate into oblivion the fact that this rise is produced by an increase in the amount of money and money substitutes. They never mention this increase. They put the responsibility for the rising cost of living on business. This is a classical case of the thief crying “catch the thief”. The government, which produced the inflation by multiplying the supply of money, incriminates the manufacturers and merchants and glories in the role of being a champion of low prices.[2]

[1] Murray N. Rothbard – What Has Government Done to Our Money? Libertarian Publishers January 1964 p 32.

[2]Ludwig von Mises, Economic Freedom and Interventionism, the Foundation for Economic Education p.94.

The conclusion is wrong. The argument is wrong.

And economists are wrong.

WHY THE ECONOMIST ARE WRONG

Inflation as measured in National statistics is not the inverse of the rate at which money is falling in value.

The value of money is what it can be exchanged for. It can be exchanged for almost anything, not just goods and services.

‘Anything’ includes assets of every kind as a previous writer at the Cobden Centre pointed out recently.

It includes bond values, equity values, property values, collectables, gold, currencies, loan books, and lots more besides.

This means that most of what economists write relating to this measure is wrong and misleading. The science is unable to advance to a higher level. Solutions which ought to be visisible are invisible.

THE CONCLUSIONS REACHED ARE WRONG

This is because the premises used are wrong.

The rate of inflation is the inverse of the rate at which money is falling in value and no one knows what that is.

This rate depends upon the levels of supply and demand.

The quantity of money is not the only factor.

When there are twice the number of people you need twice as much money.

When economies grow you need more money.

When people save more and import more you may need more money.

The article states that when new money is created by the state or by say, banks, this is a form of theft.

Sure it is. No question.

But what if the new money is distributed uniformly to everyone?

That is not theft.

Everyone is a thief? Everyone steals equally from everyone else?

Maybe it is more polite to say that everyone does some free work for everyone else.

WRONG DIAGNOSIS

So the idea that we need to manage the value of money in some precise way which is not defined does not stand up.

THE RIGHT CONCLUSION

What we do need to do is to make sure that we do not put people and businesses in harm’s way when the value of money or the quantity of money changes.

That is why I have started a new school of thought called Macro-economic Design and Management.

If the design of our markets and our contracts is good people are not harmed as money changes in quantity or value, then all which remains to be done is to manage the rate of increase in the stock of money in a way which does not disturb economic activity or wealth distribution.

That is why I have started this new school of thought called Macro-economic Design and Management.

Get the design right, make all financial plans relatively reliable and shock-proof from such issues, and the management gets good control, easily.

Found this:

http://wolfstreet.com/2015/12/27/i-was-asked-whatever-happened-to-inflation-after-all-this-money-printing/

You’ve probably seen it….