In the distant future, we might look back on 2022 and 2023 as pivotal years. So far, we have seen the conflict between America and the two Asian hegemons emerge into the open, leading to a self-inflicted energy crisis on the western alliance. The forty-year trend of declining interest rates has ended, replaced by a new rising trend the full consequences and duration of which are as yet unknown.

The western alliance enters the New Year with increasing fears of recession. Monetary policy makers face an acute dilemma: do they prioritise inflation of prices by raising interest rates, or do they lean towards yet more monetary stimulation to ensure that financial markets stabilise, their economies do not suffer recession, and government finances are not driven into crisis?

This is the conundrum that will play out in 2023 for the US, UK, EU, Japan, and others in the alliance camp. But economic conditions are starkly different in continental Asia. China is showing the early stages of making an economic comeback. Russia’s economy has not been badly damaged by sanctions, as the western media would have us believe. All members of Asian trade organisations are enjoying the benefits of cheap oil and gas while the western alliance turns its back on fossil fuels.

The message sent to Saudi Arabia, the Gulf Cooperation Council, and even to OPEC+ is that their future markets are with the Asian hegemons. Predictably, they are all gravitating into this camp. They are abandoning the American-led sphere of influence.

2023 will see the consequences of Saudi Arabia ending the petrodollar. Energy exporters are feeling their way towards new commercial arrangements in a bid to replace yesterday’s dollar. There’s talk of a new Asian trade settlement currency. But we can expect oil exports to be offset by inward investment, particularly between Saudi Arabia, the GCC, and China. The most obvious surplus emerging in 2023 is of internationally held dollars, whose use-value is set to drop away leaving it as an empty shell. It amounts to a perfect storm for the dollar, and all those who sail with it.

Those of us who live long enough to look back on these years are likely to find them to have been pivotal for both currencies and global alliances. They will likely mark the end of western supremacy and the emergence of a new, Asian economic domination.

The interest rate threat to the west’s currencies

It is a mark of how bad the condition of Western economies has become, when interest rate rises of only a few cent are enough to threaten to precipitate an economic crisis. The blame can be laid entirely at the door of post-classical macroeconomics. And like a dog with a bone, their high priests refuse to let go. Despite all the evidence to the contrary, they would now have you believe that inflation is transient after all, though they have conceded the possibility of inflation targets being raised slightly. But the wider concern is that even though interest rates have yet to properly reflect the extent of currency debasement, they have risen enough to tip the world into recession.

In their way of thinking, it is either inflation or recession, not both. A recession is falling demand and falling demand leads to falling prices, according to macroeconomic opinions. When both inflation and a recession are present, they cannot explain it and it does not accord with their computer models. Therefore, government economists insist that consumer price rises will return to the 2% target or thereabouts, because rising interest rates will trigger a recession and demand will fall. It will just take a little longer than they originally thought.

They now saying that the danger is no longer just inflation. Instead, a balance must be struck. Interest rate policy must take the growing evidence of recession into account, which means that bond yields should stop rising and after their earlier falls equity markets should stabilise. For them, this is the path to salvation. In pursuing this line, the authorities and a group thinking establishment have had success in tamping down inflation expectations, aided by weakening energy prices.

Since March, West Texas intermediate crude has retraced 50% of its rise from March 2020 to March 2022. Natural gas has fallen forty per cent from its August high. If the western media is to be believed, Russia is continually on the brink of failure, the suggestion being that price normality will return soon. And the inflationary pressures from rising energy and food prices will disappear.

What is really happening is that bank credit is now beginning to contract. Bank credit represents over 90% of currency and credit in circulation and its contraction is a serious matter. It is a change in bankers’ mass psychology, where greed for profits from lending satisfied by balance sheet expansion is replaced by caution and fear of losses, leading to balance sheet contraction. This was the point behind Jamie Dimon’s speech at a banking conference in New York last June, when he modified his description of the economic outlook from stormy to hurricane force. Coming from the most influential commercial banker in the world, it was the clearest indication we can possibly have of where we were in the cycle of bank credit: the world is on the edge of a major credit downturn.

Even though their analysis is flawed, macroeconomists are right to be very worried. Over nine-tenths of US currency and bank deposits now face a meaningful contraction. This is a particular problem earlier exacerbated by covid lockdowns and for businesses affected by supply chain issues. It gives commercial banks a huge problem: if they begin to whip the credit rug out from under non-financial businesses, they will simply create an economic collapse which would threaten their entire loan book.

It is far easier for a banker to call in loans financing positions in financial assets. And it is also a simple matter to call in and liquidate financial asset collateral when any loan begins to sour. This is why the financial sector and relevant assets have been in the firing line so far.

Central banks see these evolving conditions as their worst nightmare. They are what led to the collapse of thousands of American banks following the Wall Street crash of 1929-1932. In blaming the private sector for the 1930s slump which followed and was directly identified with the collapse in bank credit, central bankers and Keynesian economists have vowed that it must never happen again.

But because this tin-can has been kicked down the road for far too long, we are not just staring at the end of a ten-year cycle of bank credit, but potentially at a multi-decade super-cyclical event, rivalling the 1930s. And given the greater elemental forces today, potentially even worse than that.

We can easily appreciate that unless the Fed and other central banks lighten up on their restrictive monetary policies, a stock market crash is bound to ensue. And this is what we saw when the interest rate trend began a new rising trajectory last January. For the Fed, preventing a stock market crash is almost certainly a more immediate priority than protecting the currency. It is not that the Fed doesn’t care, it’s because they cannot do both. Their mandate incorporates unemployment, and their ingrained neo-Keynesian philosophies are also at stake.

Consequently, while we can see the dangers from contracting bank credit, we can also see that the Fed and other major central banks have prioritised financial market stability over increasing interest rates to properly reflect their currencies’ loss of purchasing power. The pause in energy price rises together with media claims that Russia will be defeated have helped to give markets a welcome but temporary period of stability.

The policy of threatening continually higher interest rates must be temporary as well. In effect, monetary policy makers have no practical alternative to prioritising the prevention of bank credit deflation over supporting their currencies. Realistically, they have no option but to fight recession with yet more inflation of central bank currency funding increased government budget deficits, and through further expansion of commercial bank reserves on its own balance sheet, the counterpart of quantitative easing.

Besides central bank initiatives to keep bond yields as low as practicably possible, runaway government budget deficits due to falling tax income and extra spending to counteract the decline in economic activity will need to be funded. And given that the world is on a dollar standard, in the early stages of a recession the Fed will probably assume that the consequences for foreign exchange rates of a new round of currency debasement can be ignored. While currency debasement can then be expected to accelerate for the dollar, all the other major central banks can be expected to cooperate. The point about global economic cooperation is that no central bank is permitted to follow an independent line.

The private sector establishment errs in thinking that the choice is between inflation or recession. It is no longer a choice, but a question of systemic survival. A contraction in commercial bank credit and an offsetting expansion of central bank credit will almost certainly take place. The former leads to a slump in economic activity and the latter is a commitment too large for an inflating currency to bear. It is not stagflation, a condition which according to neo-Keynesian beliefs should not occur, but a doppelgänger rerun of what did for John Law and France’s economy in 1720. The inconvenient truth is that policies of monetary stimulation invariably end with the impoverishment of everyone.

The role of credit and the final solution

To clarify how events are likely to unfold in 2023, we must revisit the basics of monetary theory, and the difference between money and credit. It is the persistent debasement of the latter which has been the problem and is likely to condition the plans for any nation seeking to escape from the monetary consequences of a shift in hegemonic power from the western alliance to the Russian Chinese partnership.

It is probably too late for any practical solution to the policy dilemma faced by monetary policy committees in western central banks today. When commercial bankers collectively awaken to the lending risks created in large part by their earlier optimism, survival instincts kick in and they will reduce their exposure to risk wherever possible. A credit cycle of boom and bust is the consequence. Inevitably in the bust phase, not only are malinvestments weeded out, but over-leveraged banks fail as well. While the intention is to smooth out the cyclical effects on the economy, the response of the state and its central bank invariably makes things worse, with monetary policy undermining the currency.

It is important to appreciate that with a sound currency system, which is a currency that only changes in its quantity at the behest of its users, excessive credit expansion must be discouraged. The opposite is encouraged by central banks. Extreme leverage of asset to equity ratios for systemically important banks of well over twenty times in Japan and the Eurozone are entirely due to central bank policies of suppressing interest rates. It is only by extreme leverage that commercial banks, which are no more than dealers in credit, can make profits from the slimmest of credit margins when zero and negative deposit rates are forced upon them.

Since bank credit is reflected in customer deposits, a cycle of excessive bank credit expansion and contraction becomes economically destructive. The solution advocated by many economists of the Austrian school is to ban bank credit entirely, replacing mutuum deposits, whereby the money or currency becomes the bank’s property and the depositor a creditor, with commodatum deposits where ownership remains with the depositor. Separately, under these arrangements banks act as arrangers of finance for savers wishing to make their savings available to borrowers for a return.

The problem with this remedy is that of the chicken and the egg. Production requires an advance of capital to provide products at a profit in due course. The real world of free markets therefore requires credit to function. And savings for capital reinvestment are also initially funded out of credit. So, whether the neo-Austrians like it or not we are stuck with mutuum deposits and banks which function as dealers in credit.

That is as far as we can go with commercial banks and bank credit. The other form of credit in public circulation is the liability of the issuer of banknotes. To stabilise their value, the issuer must be prepared to exchange them for gold coin, which is and always has been legal money. And once the issuer has established sufficient gold reserves, the issue of any additional banknotes must be covered by additional gold coin backing.

But much more must be done. Government budget deficits must not be permitted except strictly on a temporary basis, and total government spending (including state, regional, and local governments) reduced to the smallest possible segment of the economy. It means pursuing a deliberate policy of rescinding legal obligations for government agencies to provide services and welfare for the people, retaining only a bare minimum for government to function in providing laws, national defence and for the protection of the interests of everyone without favour. All else can only be the responsibility of individuals arranging and paying for services themselves. It means that most bureaucrats employed unproductively in government must be released and made available to be redeployed in the private sector productively. A work ethic perforce will return to replace an expectation that personal idleness will always be subsidised.

Given political realities, this cannot happen except as a considered response following a major credit, currency, and economic meltdown. It is a case of crisis first, solution second. Therefore, there is no practical alternative to the continual debasement of currencies until their users reject them entirely as worthless.

Money is only gold, and all the rest is credit

For a lack of any alternative outcome, the eventual collapse of unbacked currencies is all but guaranteed. To appreciate the dynamics behind such an outcome, we must distinguish between money and credit. Currency in circulation is not legal money, being only a form of credit issued as banknotes by a central bank. It has the same standing as credit in the form of deposits held in favour of the commercial banks. The distinction between money and credit, with money wrongly being assumed to be banknotes is denied by the macroeconomic establishment today. Officially and legally, money is only gold coin. It is also silver coin, though silver’s official monetary role fell into disuse in nineteenth century Europe and America.

Gold and silver coin as money were codified under the Roman Emperor Justinian in the sixth century and is still the case legally in Europe today. In English law, the unification of the Court of Chancery and common law in 1875 formally recognised the Roman position, and gold sovereigns, which were the monetary standard from 1820, became unquestionably recognised as money in common law from then on.

Attempts by governments to restrict or ban ownership of gold as money must not be confused with the legal position. FDR’s executive order in 1933 banning American citizens from owning gold did not change the status of money. Nor did similar government moves elsewhere. And the neo-Keynesian denigration of a gold standard doesn’t alter its status either. Nor do the claims from cryptocurrency enthusiasts that their schemes are a modern replacement for gold’s monetary role. As John Pierpont Morgan stated in his testimony before Congress in 1912, “Gold is money. Everything else is credit”. He was not expressing an opinion but stating a legal fact.

That gold does not commonly circulate as a medium of exchange is explained by Gresham’s law, which states that bad money drives out the good. Originally describing the difference between clipped coins and their wholly intact counterparts, Gresham’s law also applies to gold’s relationship with currency. Worldwide, unrelated societies hoard gold coin, spending currency banknotes and bank deposits first, which are universally recognised as lower forms of media of exchange. Even central banks hoard gold. And as they have progressively distanced themselves from their roles as servants of the public, they refuse to allow the public access to their gold reserves in exchange for their banknotes.

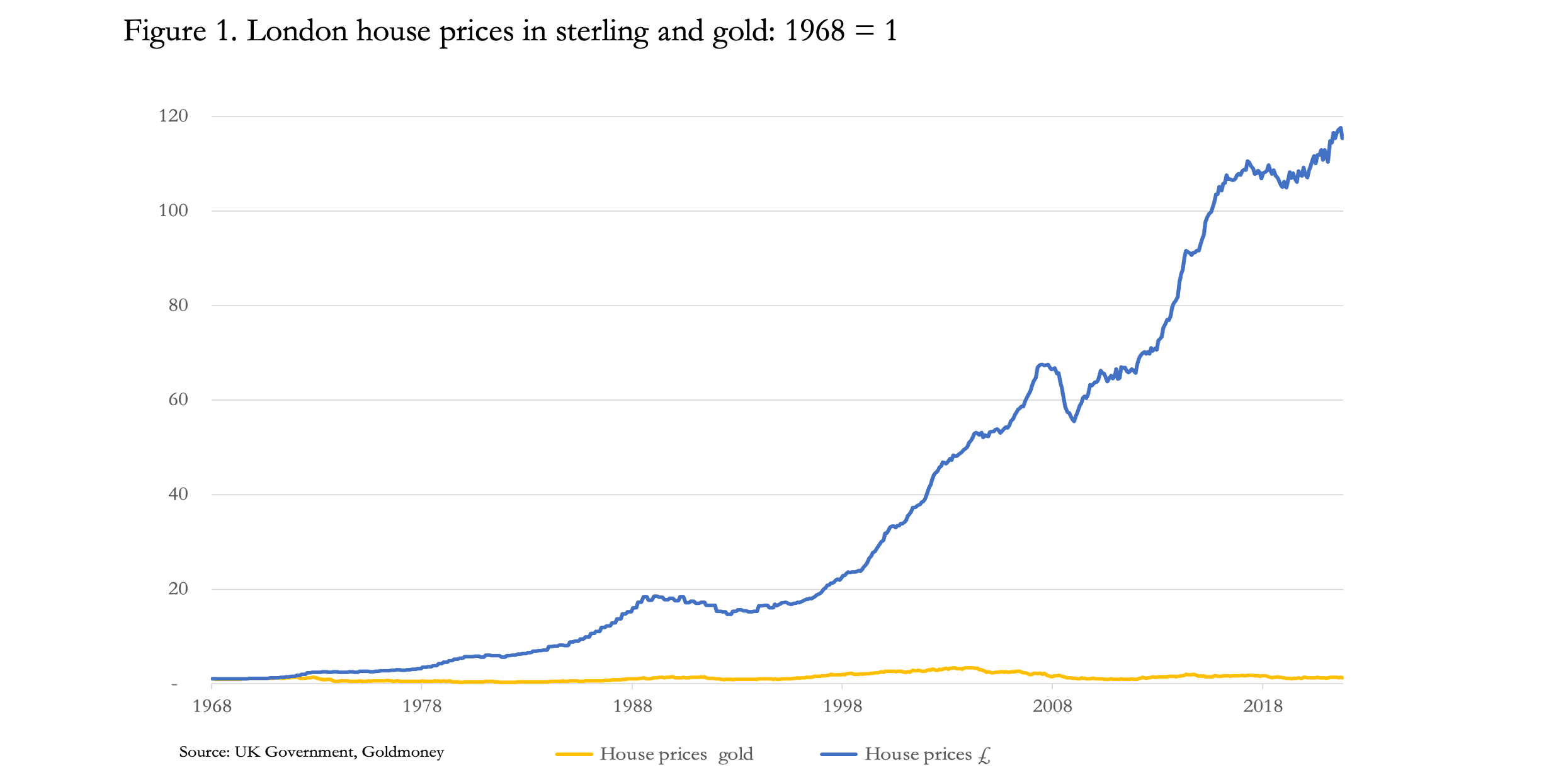

The importance of gold as a store of value, that is as sound money, appears to be difficult to understand for people not accustomed to regarding it as such. Instead, they regard it is a speculative investment, which can be held in securitised or derivative form while it is profitable to do so. When it comes to hedging a declining currency’s purchasing power, the preference today is for assets that outperform the cost of borrowing. As an example of this, Figure 1 shows London’s residential housing priced in fiat sterling and gold. Housing is the most common form of public investment in the UK, further benefiting from tax exemptions for owner-occupiers.

According to government data, since 1968 when house price statistics began median house prices in London have risen on average by 115 times. But priced in gold, they have risen only 29% in 54 years. With prices having generally risen by less outside London and its commuter belt, some areas might have seen falls in prices measured in gold.

It is virtually impossible to get people to understand the implications. They correctly point out the utility of having somewhere to live, which is not reflected in prices. They might also point out that property held by landlords produces a rental income. Furthermore, most buyers leverage their investment returns by having a mortgage.

In investing terms, these arguments are entirely valid. But they only prove that the purpose of owning an asset is to obtain a return or utility from it, with which we can all agree. The purpose of money or currency is different: it is a medium for purchasing an asset which will give you a benefit. What is not understood is that far from giving property owners a capital return which exceeds the debasement of the currency, they have just about kept pace with it. And if you had bought property elsewhere in the UK, your capital values might even have fallen, measured in real legal money, which is gold.

Since the end of the Bretton Woods agreement, the consequences of currency debasement for asset prices such as residential property have hardly mattered. The debasement of currencies has never been violent enough to undermine assumptions that residential property will always retain its value in the long run. Other assets, such as a portfolio of financial equities are seen to offer similar benefits of apparent protection against currency debasement. But we now appear to be on the cusp of a major currency upheaval. The global banking system is more highly leveraged on balance sheet to equity measures than ever before, and bank credit is beginning to contract. All the major central banks have undeclared loses which wipe out their nominal equity, affecting their own credibility as backstops to their commercial banking systems. Systemic risks are escalating, even though market participants have yet to realise it. And as economic activity turns down, government budget deficits are going to rapidly escalate. A practical remedy for the situation cannot be entertained, so the debasement of currencies is bound to accelerate. Mortgage borrowing costs are already rising, undermining affordability of residential property in fiat money terms.

The relationship between currency and real money, which is gold coin, will almost certainly break down. Measured in gold, a banking and currency crisis will have the effect of driving residential property prices significantly lower, while they could be maintained or even move somewhat higher measured in more rapidly depreciating fiat currencies.

The transition from financialised fiat currencies to… what?

There is an overriding issue which we must consider now that the long-term decline of interest rates appears to have come to an end, and that is how the dollar will fare in future. While the dollar has lost 98% of its purchasing power since the ending of Bretton Woods, it has generally been gradual enough not to undermine its role as the world’s international medium of exchange and for the determination of commodity prices. It has retained sufficient value to act as the world’s reserve currency and is the principal weapon by which America has exercised her hegemony.

It is in its role as the weapon for waging financial wars which may finally lead to the dollar’s undoing, as well as undermining the purchasing powers of the currencies aligned with it. By cutting Russia off from the SWIFT settlement system, thereby rendering her fiat currency reserves valueless, the western alliance hoped that together with sanctions Russia would be brought to her knees. The policy has failed, as sanctions usually do, while the message sent to all non-aligned nations was that America and its western alliance could render national currency reserves valueless without notice. Consequently, there has been a worldwide rethink over the dangers of relying on dollars, and for that matter the other major currencies issued by member nations of the western alliance.

At this time of transition away from a weaponised dollar, there is a general uncertainty in nations aligned with the Russian Chinese axis over how to respond, other than to sell fiat currencies to buy more gold bullion. But the sheer quantities of fiat currency relative to the available bullion suggests that at current values the bullion is not available in sufficient quantities to credibly turn fiat currencies into gold substitutes. Nevertheless, it would be logical for the gold-rich Russian Chinese axis and nations in their sphere of influence to protect their own currencies from a rapidly developing fiat currency catastrophe. So far, none of them appear to be prepared to do so by introducing gold standards for the benefit of their citizens.

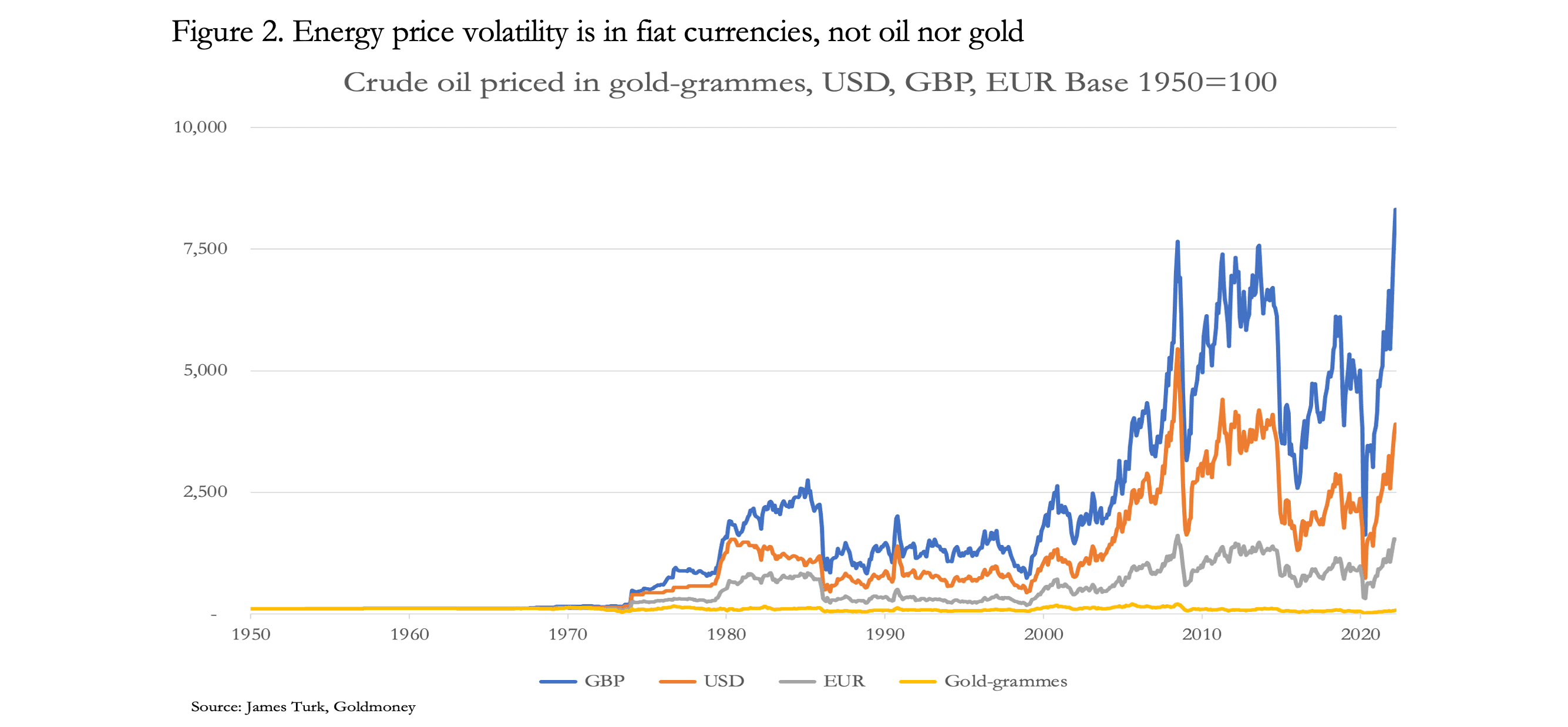

Only Russia, under pressure from currency and trade sanctions has loosely tied its rouble to energy and commodity exports. In the vaguest of terms, it might be regarded as a synthetic equivalent of linking the rouble to gold. Why this is so is illustrated in Figure 2.

Measured in fiat currencies, the oil price is exceedingly volatile, while in true money, gold, it is relatively stable. Measured in gold, the oil price today is about 20% lower than it was in 1950. Since then, the maximum oil price in gold has been a doubling and the minimum a fall of 85%. That compares with a rise in US dollars of 5,350% and no fall at all. Undoubtedly, if gold had traded free from statist intervention and speculation in currency and commodity markets and from the effects of fiat-induced economic booms and busts, the price of oil in gold would most likely have been even steadier.

By insisting that those dubbed by Putin as the unfriendly nations must buy roubles to pay for Russian oil, demand for roubles on the foreign exchanges became linked to demand for Russian oil, which in turn is linked more closely to gold than the unfriendlies’ currencies. But it seems that in official minds, making this link between the rouble, oil, and gold is a step too far. When it comes to replacing the dollar with a new trade currency for the Asian powers, their initial discussions have suggested a more broadly based solution.

The Eurasian Economic Union (EAEU), consisting mainly of a central Asian subset of the Shanghai Cooperation Organisation (SCO) earlier this year announced that plans for a trade settlement currency were being considered, backed by a mixture of commodities and the currencies of member states.

So far, members of the SCO have restricted their discussion to ways of replacing the dollar for the purpose of transactions between them, a long-term project driven not so much by change in Asia but by US trade aggression and American hegemonic dollar policies over time. Following Russian sanctions imposed by the West, it is likely that the dangers of an immediate dollar crisis are now being more urgently addressed by governments and central banks throughout Asia.

With the West plunging into a combined systemic and currency crisis, no national government outside the dollar-based system appears to know what to do. Only Russia has been forced into action. But even the Russians are feeling their way, with vague reports that they are looking at a gold standard solution, and others that they are considering Sergey Glazyev’s EAEU trade currency project. As well as heading a committee set up to advise on a new trade settlement currency, Glazyev is a senior economic advisor to Vladimir Putin.

From the little information made available, it appears that Glazyev’s EAEU monetary committee is ruling out a gold standard for the new trade currency. Instead, it has been considering alternative structures without achieving any agreement so far. But for the project to go ahead, proposals reported to include national currencies in its valuation basket must be abandoned. Not only is this an area where Glazyev is unlikely to obtain a consensus easily from member states, but to include a range of fiat currencies is unsound and will not satisfy the ultimate objective, which is to find a credible replacement for the US dollar for cross-border trade settlements. For confidence in the new currency to be maintained, the structure must be both simple and transparent.

Since the currency committee’s press release earlier this year, there have been further developments likely to influence it construction. Led by Saudi Arabia, the Gulf Cooperation Council is turning its back on the dollar as payment for oil and gas. Again, this development is attributable to climate change policies of the US-led western alliance. Not only has the alliance demonstrated that foreign reserves held in its fiat currencies can be rendered valueless overnight, but climate change policies send a clear message that for the GCC the future of their trade is not with the western alliance. For long-term stable trade relationships, they must turn to the Russian Chinese axis.

It is happening before our eyes. China has signed a 27-year supply agreement with Qatar for its gas. President Biden attempted to secure a agreement with Saudi Arabia for additional oil output. He left with nothing. President Xi visited earlier this month and secured a long-term energy and investment agreement, whereby Saudi’s currency exposure to the yuan is minimised through Chinese capital investment programmes in the kingdom

Already, an increase in China’s money supply is an early indication that propelled by cheap energy and infrastructure investment programmes, her economy is in the early stages of a new growth phase, while the western alliance faces a potentially deep recession. The currency effect is likely to be supportive of the yuan/dollar cross rate, which the Saudis are likely to have factored into their calculations. But they will almost certainly need more than that. They will want to influence settlement currencies for the balance of their trade. Their options are to minimise balances on the back of inward investment flows, as mentioned above. They can seek to influence the construction of the proposed EAEU trade settlement currency. Or they can build their gold reserves, to the extent they might wish to hedge currencies accumulating in their reserves.

For the western alliance, the death knell for the petrodollar means that 2023 will see a substantial reduction of dollar holdings in the official reserves of all nations in the Russian Chinese axis and those friendly to it. The accumulation of dollars in foreign reserves since the end of the Bretton Woods regime is considerable, and its reversal is bound to create additional difficulties for the US authorities. Foreign owned US Treasuries are starting to be sold, and the $32 trillion mountain of financial assets and bank deposits are set to be substantially reduced. The potential for a run on the dollar, driving up commodity input prices in dollars, is likely to become a considerable problem for both the US and the entire western alliance in 2023.

Conclusion

We have noted the deteriorating systemic and monetary prospects for fiat currencies, predominantly those of the dollar-based Western currency system. Both sound economic and Marxist theory indicates that a final crisis leading to the end of these fiat currencies was going to happen anyway, and the financial war against Russia has become an additional factor accelerating their collapse.

After suppressing interest rates to zero and below, rising interest rates are finally being forced upon the monetary authorities by markets. With good reason, it has become fashionable to describe developments as an evolution from a currency environment driven by and dependent on financial assets into one driven by commodities — in the words of Credit Suisse’s Zoltan Pozsar, Bretton Woods II is ending, and Bretton Woods III is upon us.

For this reason, there is growing interest in how a new world of currencies based somehow on commodities or commodity-based economies will evolve. This year, Russia successfully protected its rouble by linking it to energy and commodity exports and in the process undermined Western currencies.

While it is always a mistake to predict timing, the fact that no one in the financial establishment is debating how to use gold reserves to protect their currencies clearly indicates that we are still early in the evolution of the developing fiat currency crisis. Officially at least, the forward thinkers planning a new pan-Asian trade settlement currency alternative to the dollar are looking at backing it with commodities and not a gold standard. Since Sergei Glazyev announced an enquiry into the matter, the Middle Eastern pivot away from the petrodollar to Asian currencies not only injects a new urgency into his committee’s deliberations but is bound to have a significant bearing on its outcome.

The implications for the western alliance play no part in current monetary policies. Their central banks act as if there’s no danger to their own currencies from these developments. But any doubt that fiat currencies will be replaced by currencies linked to tangible commodities, whether represented by gold or not, is fading in the light of developments.

With neither the economic establishment nor the public having a basic understanding of what is money and why it is not currency, it is hardly surprising that current financial and economic developments are so poorly understood, and the correct remedies for our current monetary and economic conditions are so readily dismissed.

These errors and omissions are set to be addressed in 2023.