It was Keynes’ offhand dismissal of Say’s law, or the law of the markets, in 1936 which is leading us into an economic and monetary crisis.

It was dismissed by him to invent a role for the state.

That is why Keynes is so popular in the mainstream establishment. By dismissing market reality, he invented a whole new branch of economics. Macroeconomics exchanged statistics and mathematics for human action, the prospect of centralised management substituted for ambiguity.

In this article I look at the flaws in macroeconomics, the state theory of money (an old recurring theme from John Law onwards), misleading statistics measured in unhinged fiat currencies, and why Keynesian fears of a general glut are misplaced — all of which stem from the error of dismissing Say’s law.

Importantly, Say’s law ties the volume of production to demand, so policy makers who believe a recession will kill price inflation, and therefore allow central banks to reduce interest rates, are simply wrong.

The state-educated mainstream is so sold on macroeconomic theories and the state management of economic outcomes that reasoned debate gets no traction. The only solution is for a final economic and monetary crisis to bring an end to all macroeconomic dogmas.

The origin of macroeconomics

Jean-Baptiste Say wrote his ground-breaking book on economics in 1803, revising subsequent editions. His Traité D’économie Politique, as it is known in French in short form, described the division of labour and the role of money as the agent for turning specialised production into general consumption. It became known as Say’s law or the law of the markets, and was the first commandment of classical economics, until Keynes persuaded us otherwise in his General Theory published in 1936.

Keynes denial of Say’s law was in the spirit of Humpty Dumpty — ″’When I use a word, it means just what I choose it to mean – neither more nor less”. He rewrote economic definitions to suit his thesis. Humpty Keynes redefined economics to exclude the inconvenient reality of Say’s law, along with many others that logically followed from it. It was necessary for Keynes to deny it in order to ease in a role for the state, allowing governments to intervene in the relationship between production and consumption. The invention of macroeconomics, which played down the unpredictable human element expressed in markets, in favour of statistics and mathematical analysis, can be traced to Chapter 3 in his General Theory, where he wrote:

“If, however, this is not the true law relating the aggregate demand and supply functions, there is a vitally important chapter of economic theory which remains to be written and without which all discussions concerning the volume of aggregate employment are futile.”

Say’s law was summarily dismissed, hardly mentioned again in his seminal work. The whole basis of Keynes’s new macroeconomics, that vitally important chapter of economic theory which remains to be written, boils down to that one little word, “If” heading the quote above. “If” is a supposition and certainly not evidence leading to the discovery of an entirely new branch of economic science. It was a simple trick, dismissing the inconvenient truth early in his thesis so that he could proceed to construct a fantasy. Keynes should have been dismissed as a quack, like John Law who propounded similar theories and ruined France in 1720. And Georg Knapp, a German economist of the Historical school, who published his state theory of money in 1905, arguably encouraging the Kaiser’s government to build up armaments before the First World War at no visible cost to the people, and to continue to finance itself by inflationary means after Germany’s defeat.

Yet with Keynes’s little “if”, here we are nearly ninety years later still travelling along his intellectual rails full tilt into the buffers of economic destruction. The reasons why Law, Knapp, and now Keynes and their theories rose from obscurity to fame are that their theories appeal to governments, seemingly conferring on them an economic role, enhancing their control over their citizens, and therefore the justification for increased power and revenues. The last thing they will consider is that these theories are flawed, until the evidence of a final crisis forces them to face up to their fallacies.

Despite Keynes’s intellectual fraud, the division of labour and the role of money cannot be denied. But the world has moved on from the simpler world of J-B Say. At the time of the French Revolution when he was observing the economic activities of people, tradesmen probably refused to take credit for payment, accepting only gold and silver coin because paper assignats followed by mandats territoriaux were successively descending into worthlessness.

Plus ça change, plus c’est le même chose! Today, under neo-Keynesian policies directed by the state, it is only forms of credit that intermediate between our production and consumption, and coins are only tokens. Over two centuries ago in rural France, consumption for most was more a question of survival than access to the luxuries we are familiar with today and reckon to be our right. Production was basically local, whereas today it is global. And we now have factories, when few existed in the predominantly agricultural economies of Say’s time because the industrial revolution in France had barely started.

Yet, despite all these differences Say’s central proposition linking production to consumption and ruling out a general glut of goods due to a collapse in consumption still holds. No employment, no demand. No demand, no employment.

However, rehabilitating Say’s law into modern economics must take account of today’s economic and monetary conditions. Neo-Keynesians ignore the consequences of credit’s loss of purchasing power in their static models. This may confuse the issue for them, but Say’s law still holds whether transactions are in money or credit. Here, we are defining legal money as a medium of exchange without counterparty risk — gold and gold coin. Now that we have only fiat currencies whose values in terms of goods are continually deteriorating, statistical evidence is worthless — despite macroeconomists treating long runs of price and related data as if the purchasing power of a fiat currency is constant over time. I have more to say on this below.

In the days of sound money and the credit which took its value from it, we could see the consequences of economic progress and regression on both individual prices and also their general level. Today, we labour under the delusion that what we knew to be true under sound money still applies to unsound fiat currencies and their dependent credit. In all our statistical comparisons we therefore believe that all price changes still come from the values of goods and services. And by dismissing Say’s law, we dismiss the certainty that the purchasing power of unanchored credit will continue to decline even in a recession. So, what are the true consequences of a deteriorating economic condition for prices in a modern economy?

It is far from a simple matter, but as a starting point we can sensibly argue three points. First, just as Keynes dismissed Say’s law in order to create an economic role for the state, its rehabilitation must reject his supposition entirely and everything that flowed from this error. Secondly, that with the dismissal of the state from economic functions, macroeconomic statistics gathering can only have restricted validity, and economic modelling must be dismissed entirely. And thirdly, in economic conditions leading to unemployment not only does consumption decline but production will as well because the unemployed are no longer producing. In other words, there is no such thing as a Malthusian glut, and the hope in some quarters that price inflation will diminish in a recession as demand contracts will be disappointed.

The rest of this article looks at the major issues arising from the Keynesian dismissal of Say’s law — the law of the markets.

The errors in modern socialism

Perhaps the starkest example of the difference today between a state controlled economy and a relatively free capitalist one is found in the contrast between the two Koreas. In the North, they are starving. In the south, people of the same ethnicity are prospering. This is not just a fluke. In the late 1940s, China was descending into communism and abject poverty while Hong Kong rose from the ashes of Japanese occupation and the collapse of the military yen into capitalist prosperity with no natural resources of its own. Concurrently with China and Hong Kong, East and West Germany exhibited the same phenomenon until freedom of movement between the two returned.

The empirical evidence of these failures and success are put down to communist extremism by historians and today’s politicians in the western alliance, and they say are different from democratic socialism. But apologists for state intervention and control can argue as much as they like that communism is different from democratic socialism, but they cannot explain away the fact that communism is simply socialism in extremis sharing the same basic flaws as socialising democracy.

Understanding why this is the case is hampered by the superficial attraction of organisational planning applied to spontaneous markets. The former appeals to a surface form of logic, while the latter lacks a ready explanation. This riddle was laid bare by the great economist of the Austrian school, Ludwig von Mises in his Socialism: An economic and sociological analysis. The essence of the argument was contained in a further essay, Economic calculation in the socialist commonwealth, written in 1920 and a hot topic at the time. In that essay, Mises laid down the reasons why economic management and intervention by the state would always fail. As the Russian economist, Yuri Maltsev put it, “Mises exposed socialism as a utopian scheme that is illogical, uneconomic, and unworkable at its core.” Maltsev confirmed this from his personal experience as an economist in the Soviet Union.

The difference between communism and democratic socialism can be likened to the fate of a lobster plunged into boiling water compared with that of a frog, who in the modern cliché is cooked from cold. The relative level of authoritarianism is different from the outset but ends up being similar in its final outcome. The demonstrable failures of democratic socialism have led to ever-increasing restrictions on markets, inching it ever closer to communism. The common denial of capitalism and the profit motive as being somehow immoral is part of the pro-state and anti-market propaganda.

The reason the state always fails in its attempt to manage the economy is partly due to its objectives being political in nature rather than economic, and partly due to the impossibility of it entering into economic calculation. It was the latter point which Mises explained so well in his 1920 essay. Irrespective of the politics, it is impossible for a state which owns the means of production in its central planning to know in advance whether its output will be demanded by consumers. Some of it might well be, but assessing the level of demand in the planning of production is impossible. And the state cannot assess the evolution in a product to ensure it will be freely demanded in future. The state therefore resorts to monopolistic behaviour to enforce consumption.

By way of contrast, the capitalist in a free market will use his specialist knowledge to assess demand and seek to respond by supplying his product to consumers profitably. For him, the customer is king. If he fails, he either cuts his losses, or adapts the product to satisfy consumer demands. Production methods and output evolve to satisfy demand, which together define progress. While the state is unable to evolve its production satisfactorily and therefore lacks the fundamental ability to foster economic progress, capitalists seeking profits in free markets improve economic conditions and standards of living wholly in accordance with Say’s law. In other words, through specialisation the entire cohort of independent manufacturers and service providers together satisfy the general and evolving demands of the markets.

As a matter of reluctant practicality, social democracy permits capitalism to exist. In common with the early fascist policies of Mussolini, capitalism is tolerated so long as it can be controlled by the state. This control is achieved through extensive product regulation, by partial nationalisation of the economy, and by virtue of the fact that state spending is the largest single element in a social democratic economy. This spending is not funded out of production, but by taxes imposed on producers and consumers. A socialising state is promoted as a benefit for society as a whole, but the reality is that is an economic burden in proportion to its size.

Under the aegis of social democracy, the economy becomes increasingly directed away from market freedoms, and it performs progressively less than its potential to improve the living conditions of the population. The economy’s underperformance is invariably blamed upon the private sector by the state when it is the consequence of the state’s own interventionalist policies.

How statistics mislead us all

The division of labour means that it is always the individual who deploys his or her skills in order to consume — consumption which is personal to the needs and desires of the individual. While there are needs common to each individual, the consumption of which goods and services an individual actually desires cannot be forecast by any observer. Much of tomorrow’s demand is spontaneous and is not even known to individual consumers in advance.

Even if they are accurate, the gathering of statistics measuring this demand can only be of its past history. It is a gross error to think that demand statistics valid in the past can be projected into the future and retain any true relevance. We see this in the continual failure of economic modelling and econometric forecasts. It is one thing for an economist to further his understanding of a branch of human science, as a branch of psychology, and another to assume it is a natural science, such as physics or biology. The former cannot be averaged and predicted, while the latter can be statistically quantified. No wonder Keynes, whose primary discipline was mathematics, preferred to dismiss Say’s law in favour of mathematical and statistical analysis.

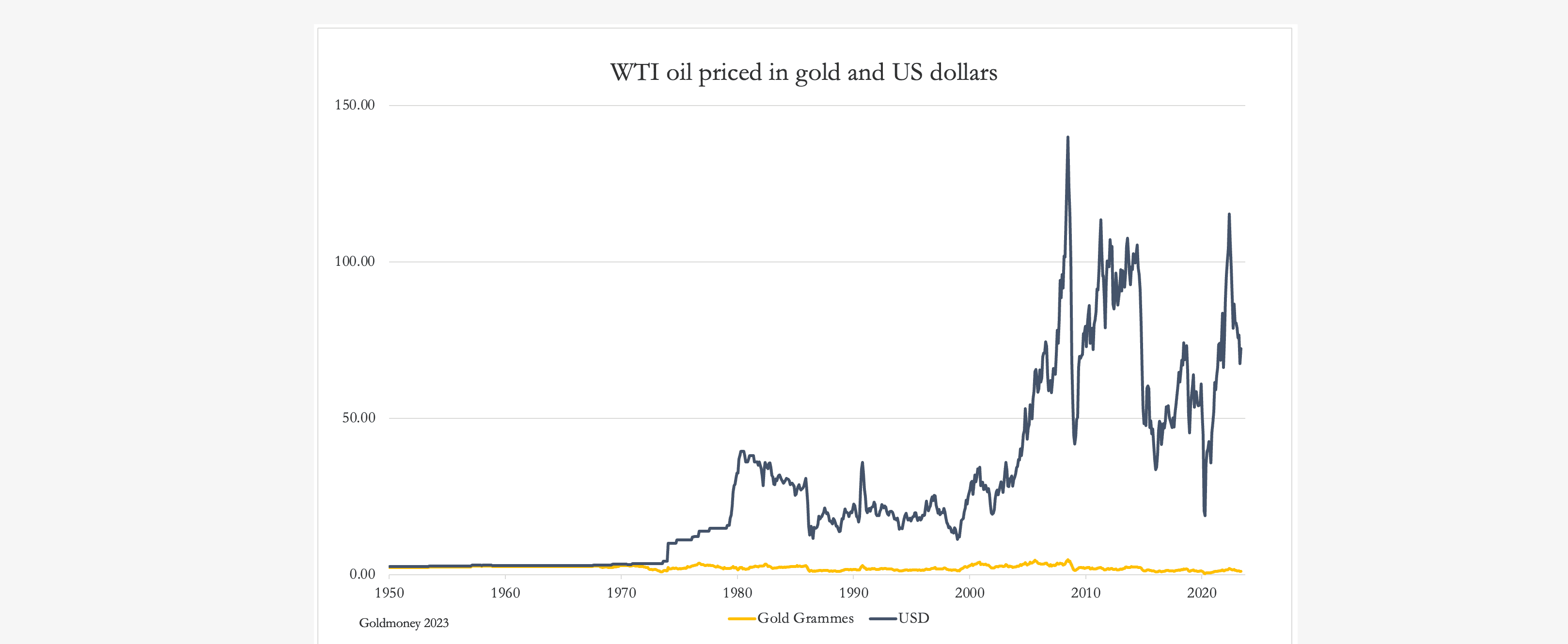

Mention has already been made above of the mistake in comparing prices of goods and services over time valued in fiat currencies. The chart below of WTI oil, a basic unit of energy upon which almost the entire global population depends, illustrates the enormity of this mistake.

The two prices are in legal money, which is gold, and in fiat dollars, which is currency. Since 1950, when the price of WTI oil was $2.57 per barrel and in gold grammes it was 2.28, in dollar terms the price has soared to around $70 today, a multiple of over 27 times. Yet in gold, it is 1.14 grammes, having exactly halved. In legal money the price has been considerably less volatile than in dollars. The riddle posed to us by this chart is which price should be used for valuing oil — a depreciating and volatile dollar, or a relatively stable legal and sound money?

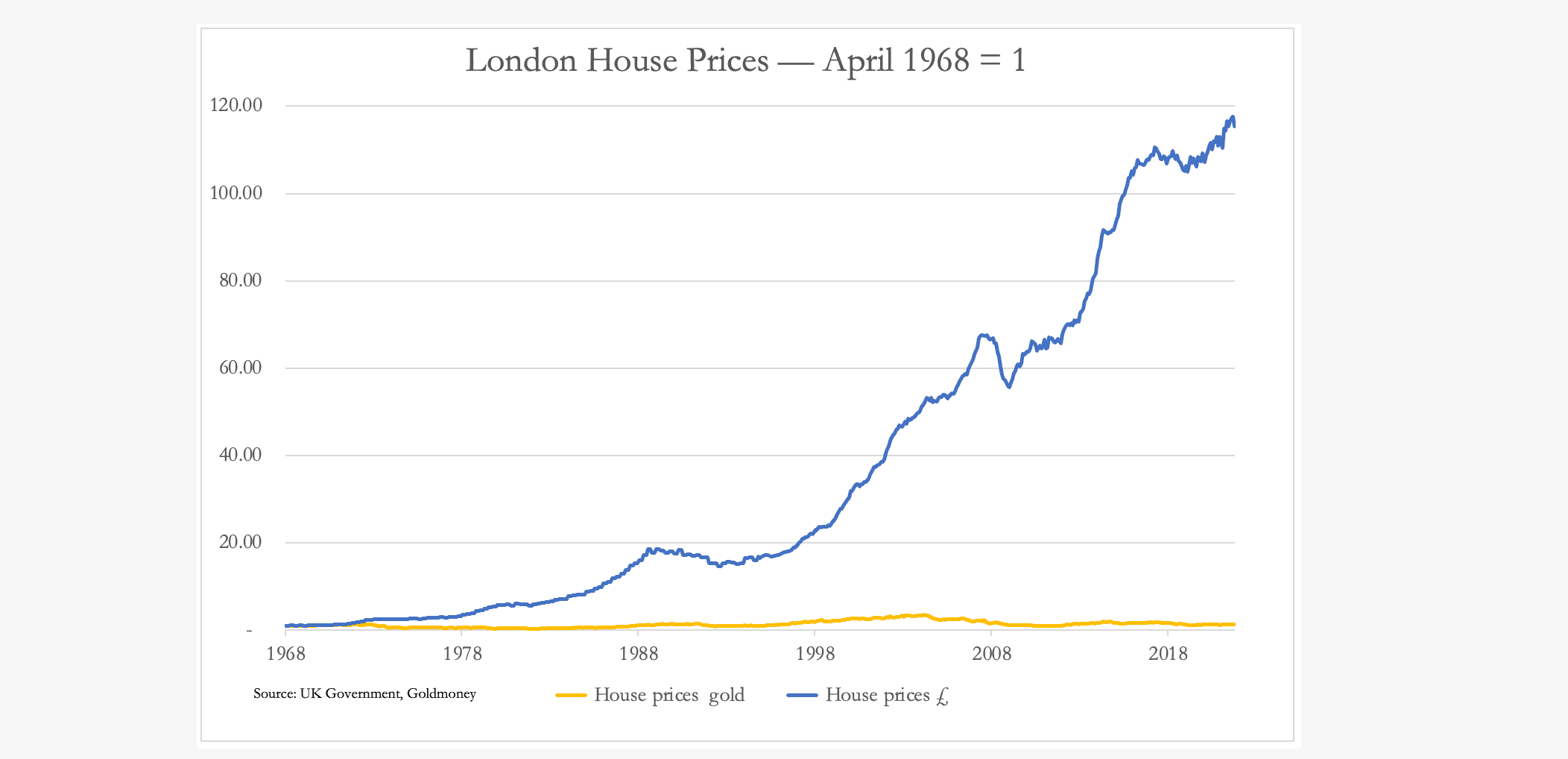

Clearly, it is long-term dollar price comparisons which are badly flawed. Yet market traders, proud to call themselves macroeconomists without understanding the implications of the term, maintain their long-term charts of oil and other commodities in dollars wholly unaware of their falsity. Furthermore, everything which can be traded is valued in fiat dollars and other currencies, from financial assets to housing. The next chart is of residential property in London, priced in pounds and gold.

Anyone who observes the residential property market in the UK will tell you what an excellent investment it has been, nowhere more so than in London. But this statement only holds for a fiat pound, which since 1968 has lost over 99% of its purchasing power measured in real legal money, which is still the gold sovereign coin. Today, the value of London residential property in gold has risen by a paltry 14% since 1968, compared with 116 times in depreciating pounds. Yet, the plain facts are met with widespread disbelief.

Under the fiat currency regime, values of everything are a flawed concept, reflecting not changes in subjective values so much as that of declining fiat currencies. But this statistical legerdemain which fools everyone extends to other areas of the statistical universe. Labour productivity analysis is a nonsense because of the underlying assumptions, and the lack of consideration of the costs to an employer of employment and other labour taxes. The approach is always from the statist viewpoint, whereby politicians wish to see higher output per worker promoting higher tax returns. It is never that of an employing businessman who is the only true assessor of the costs and benefits of employing the various forms of labour in his enterprise profitably.

GDP and government spending

To confuse gross domestic product with economic growth, itself a meaningless term when economic progress is implied, is a further error. Governments are fixated on GDP, which must always grow. GDP is not economic growth, but growth in the total currency value of transactions, usually over the course of a year or annualised.

If the currency is debased by its inflationary issuance, nominal GDP increases to the extent that debasement feeds into the GDP statistic. Inflation of the currency is particularly associated with increased government spending, so virtually all the increase in it fuels GDP. In the past, governments have regularly outperformed market expectations of GDP growth by the simple expedient of increasing government spending. Investors failing to understand this trick see it as positive, and stock markets rise on the news. GDP is only good for allowing a government to estimate prospective tax income. Otherwise, it is a useless and misleading statistic.

As stated above, GDP is routinely and unconsciously confused with economic progress. But a moment’s reflection will show that progress cannot be statistically measured. Progress is a concept which at its fundamental level is an improvement in a person’s living standard. There is no doubt that entertainment technology, in the form of televisions, gaming computers, and other electronic equipment all of which have fallen in price have improved many people’s enjoyment immensely. GDP incorporating declining prices for these products is bound to undervalue these benefits, and by classifying their prices as deflationary might even claim they detract from economic growth. Yet, government spending which is funded by removing purchasing power from producers and consumers and is therefore a brake on progress is classified as positive due to its inclusion in GDP.

During the covid crisis, when much of the productive economy shut down UK government spending rose to about 50% of GDP, though since then it has declined to an estimated 43% in the last fiscal year (to April 5th, 2023). Similar increases occurred in other nations. In Europe, French government spending peaked at 61.3% of its economy in 2020, declining to 58.1% last year. In Italy it was 57% and 56.7% respectively, and in Spain, 52% and 47.8%. With these levels of state spending, when analysing GDP it is extremely important to decide how to treat it.

Government economists are bound to argue that government spending is important in economic terms, and that GDP growth must include it. Furthermore, on a consumption basis it is argued that spending by government employees must be included, as well as government demand for goods and services. While this might appear to be a valid point, it misses the bigger picture.

While it is true that state employees’ and departmental spending are part of the total economy, the state’s taxes which fund them reduces income available for consumption for those not employed by the state. Government spending as a whole replaces it with the provision of services not freely demanded, which is fundamental to the benefits which flow from Say’s law — the law of the markets.

You don’t have to look far for examples of how state spending is a burden on overall economic activity, and that the successful economic approach is to free up the private sector, eliminating government and its intervention as much as possible. It is this approach which led to the remarkable success of Hong Kong in the post-war decades, compared with the poverty inflicted on the same ethnic people on the mainland under Mao Zedong where government was 100% of the economy.

Convincing the establishment that inflating GDP ends up suppressing economic progress is an uphill struggle. Instead of accepting the empirical evidence, governments routinely use their tax-raising powers to increase economic intervention, spending as a proportion of the whole, and debasing the currency by deliberately running budget deficits.

This leads to a conflict between politicians seeking to represent the electorate’s interests and the state itself. Politicians on the right vying for office are usually free marketeers with ambitions to reduce the state’s presence as a proportion of the total economy. They are appointed with a zeal to take an axe on spending and bureaucracy, but there are good reasons why they never achieve it. When they gain ministerial responsibility, their priority changes to protecting their budgets from being reduced, because cuts in departmental spending amount to a loss of power. Therefore, to the extent that any savings on spending are achieved, ministers always want to come up with other plans to maintain or increase funding levels. The negative economic consequences simply rack up, and the government’s share of GDP inexorably tends to increase.

This is the true legacy of confusing GDP with economic progress. While the transactions that together make up a GDP total can be measured, their true value in terms of the satisfaction and the progress in the quality of life they provide cannot. The only way in which they can be measured is by each individual in a community and nation, and not by those who claim to represent them.

Why there cannot be a general glut

The Keynesian error of believing that a recession leads to a general glut, and therefore a fall in the general level of prices, has its origin in the 1930s depression. But it is obvious that under the conditions of the division of labour, whereby people are employed to produce so that they can consume, this cannot be true in a general sense, because production must decline as well as consumption when unemployment rises. In other words, a general glut of unsold produce cannot arise, because the unemployed are no longer producing.

Nevertheless, Keynesian fears of a glut when a recession occurs and unemployment rises leads modern governments to create demand in a recession by increasing welfare benefits. According to the Keynesian playbook, this funding is stimulative by means of inflationary deficits, intended to help stabilise prices as demand weakens. But without a general glut and a stable currency the overall level of prices is unlikely to change significantly in real terms when there is no government intervention because of Say’s law.

Modern governments intervene by deficit spending without contributing to production. Instead of a recession leading to surplus production, government spending leads to surplus demand. This explains how the inflationary effects of Keynesian stimulation can lead to significantly higher prices, even in a slump, as was seen in Britain’s inflationary crisis in the mid-1970s. It is also entirely consistent with the factors driving an economy into a slump during a currency’s collapse, such as witnessed in the European inflations in the early 1920s.

So, what happened in the 1930s, disproving Say’s law in the minds of the neo-Keynesians?

The first error in their analysis was not understanding the consequences of the inflationary 1920s. They were fuelled by the Fed’s expansionary monetary policies under the leadership of Benjamin Strong, and President Hoover’s anti-capitalist, interventionist policies at the peak of the credit cycle. The inevitable consequences were a speculative bubble followed by a financial crisis between late-1929 and 1932 which wiped out thousands of banks and their credit, which were the backbone to maintaining economic activity. And this was followed by Hoover’s heavy handed interventionism.

Hoover also raised income taxes significantly to fund his interventions. Despite these increases, during Hoover’s tenure the Federal Government’s deficit to GDP soared from a 0.7% surplus to a 6.4% deficit and these deficits continued under Roosevelt, though they lessened as the banking crisis passed.

Not only did banks go bust in their thousands, but there were other factors. The Smoot-Hawley Tariff Act, which built in higher tariffs on top of those of the Ford McCumber tariffs of 1922, was signed into law by President Hoover in 1930. So, not only was bank credit in the economy imploding, but including tariffs the prices of imported goods and therefore the production costs of most American manufactured products were raised to uneconomic levels. It was a fatal combination, because little could be produced profitably at a time when there was little or no bank credit available. Consequently, US GDP contracted from $103.6bn in 1929 to $56.3bn in 1933. This was not the same thing as a general glut, because demonstrably both production and consumption contracted. Primarily, it reflected a collapse in bank credit.

While credit had become freely available in the previous decade, the introduction of tractors and other farm machinery had led to a massive expansion of agricultural output. Prices of agricultural produce, which were already declining due to oversupply, were bound to fall even more when credit was withdrawn by failing local banks in America. The farming community was forced to sell its output at anything they could get for it, because of the lack of credit.

This was a specific market adjustment at a time when worldwide cereal and other agricultural output prices were falling due to overproduction. The slump in prices attributable to the banking crisis hit farmers particularly hard, not just in America but worldwide through values reflected on the commodity exchanges.

Because American farmers were forced sellers of their agricultural output, it was later assumed by Keynes and other economists that there was a glut and that Say’s law was therefore flawed. But the mistake was to miss the links between the collapse in bank credit from bank failures, the pressure on farmers to dump their product at any price, and the coincidence of global overproduction due to the rapid advances made in mechanisation in the previous decade.

The causes of the 1930s depression and its longevity were clear — you need look no further than empirical evidence. Long before Keynes traduced Say’s law, both Hoover and Roosevelt with his New Deal made the depression considerably worse than it would otherwise have been, acting as proto-Keynesians. It was the first time that the Federal Government had intervened in what would otherwise have been two or three years of economic and credit hiatus, which had been the experience of previous episodes. The previous depression in 1920—1921 lasted only eighteen months without statist intervention. Before President Hoover’s tenure, it was generally acknowledged that intervention only made things worse, and that left alone, a slump in business activity would correct itself.

Economists subsequently formulating statist policies badly misread the causes of a slump. They still fail to appreciate that there is a cycle of bank credit, identified by economists of the Austrian school as a business cycle. It is caused by bankers acting as a cohort increasing the quantity of credit to a point when their balance sheet exposure becomes excessive relative to the bankers’ own capital, and they then try to reign in their balance sheets. This is not a conspiracy between bankers, but reflects their human behaviour, and is cyclical in nature. It can be traced for so far as reasonable records exist, in the UK as far back as the end of the Napoleonic wars. And it is a cycle of credit expansion and contraction averaging roughly ten years.

Even for economists, it is always easier to observe the evidence of an economic downturn than its underlying cause. In all the voluminous analysis of the great depression, the cycle of bank credit is hardly mentioned. Only economists of the Austrian school have pointed out that the depression was the natural consequence of excessive credit expansion in the previous decade. And Keynes’s followers with their mathematical and statistical macroeconomics are still blind to the role of bank credit underlying booms and slumps. They think they can model the economy, steering it from one objective to another by supressing free markets. But they cannot model human bankers’ balance of greed for profit and fear of losses.

Economic and monetary policies ignore Say’s law — the law of the markets — persisting in their failed interventions. The response to failure is usually to claim that the error was to not intervene enough. A feature of these failures is for policy makers to seek solace with their international counterparts, doubling down in a group-thinking effort to achieve statist objectives.

The errors in currency management

This week, the persistence of consumer price inflation in the UK has even led a member of the Monetary Policy Committee to say that interest rates will have to be raised to the extent that the UK economy enters a recession. But with broad money supply, no longer expanding, we can see that there’s something wrong with his analysis. At the same time, all commentary on stubborn price inflation is about too much demand for too few goods. Changes in the purchasing power of the currency are never mentioned. While individual prices fluctuate, when the general level of prices increases it can only be because of changes in a currency’s purchasing power.

There is only one reason why the purchasing power of a fiat currency changes, and that is in the behaviour of its users. By adjusting the relationship of their immediate liquidity to their spending, collectively they can have a profound impact on its purchasing power. This is why the state theory of money fails, and the monetary authorities always fail to control the purchasing power of their fiat currency. A currency must be anchored to real money, which is gold coin.

When banknotes were fully exchangeable for gold coin, their purchasing power remained constant irrespective of the quantity in circulation. But banknotes are typically less than a tenth of the circulating medium, the balance being bank credit. The relationship between bank credit and banknotes is almost parity. Therefore, so long as counterparty risk between a bank’s depositors and the bank is not an issue, bank credit will always take its value from the currency. It is the currency which must be credible.

In the first of the two charts above of WTI oil priced in dollars and gold, we can see that the price of oil in dollars was stable between 1950 and 1970, when the dollar price increased from $2.57 per barrel to an average of $3.35. At that time, the dollar was loosely tied to gold through the Bretton Woods agreement, with only national central banks and organisations such as the IMF able to exchange dollars for gold. During that time, M3 money supply increased from $172bn to $750bn, an increase of 336%.

This was not the only example. Between 1844 (the time of the Bank Charter Act) and 1900, the wholesale price index was unchanged, and it was also remarkably stable over that time fluctuating little. But between 1844 and 1900, the sum of Bank of England banknotes in circulation and commercial bank deposit obligations increased eleven times —almost entirely bank credit with the Bank of England’s note issue being little changed — and there was a material increase in the quantity of short-term, commercial bills funding foreign trade as well. Monetarist theory would suggest that the expansion of credit on such a scale would undermine the purchasing power of the currency, but plainly it did not.

The reason the expansion of bank credit need not undermine a currency’s purchasing power is that so long as the level of credit is genuinely demanded by economic activity instead of financing excess consumption, its expansion does not drive up prices. The source of excess consumption is to be found in government deficit spending because individuals always have to settle their debts while a government does not. As mentioned above, governments can always resort to deficit spending.

From this we know that government fiscal and monetary policies coupled with its fiat currency are the sole reasons behind a deteriorating purchasing power for its currency. Indeed, the Keynesians deliberately target a continual rate of debasement reflected in a CPI inflation rate of 2% by using monetary policy in an attempt to regulate credit demand.

The solution: leave markets alone and bring back sound money

If monetary stability is to return, all attempts by governments to manage private sector outcomes which have always failed and will continue to do so must be abandoned. And sound money, that is to say a gold coin standard freely available to ordinary people at their choice must be re-established. Interest rates would then stabilise at risk-free annual rates of just a few per cent set by markets in the context of demand for investment capital and the availability of savings. Market stability will automatically follow. The diversion of human activity into speculation will diminish, benefiting the economy from its redeployment into more productive pursuits. No longer would we have governments attempting to chase monetary objectives which bankrupt homeowners with mortgages as a result of misguided Keynesian policies.

A return to sound money clips the wings of high spending politicians, but other specific changes must also be introduced, reversing Keynesian macroeconomic policies entirely:

- Government spending must be reduced substantially, with an initial target for it to be no more than 20% of the economy. This will reduce the tax burden on productive businesses and workers for the benefit of non-inflationary progress. It will require extensive legislation to be passed eliminating mandated spending commitments.

- The policy of regulating goods and services must be abandoned, and responsibility for judging product suitability handed back to individuals.

- All taxation must be removed from savings, interest earned, and capital gained: savings will have already been taxed when earned. Savings are the necessary source of investment funding for economic progress. And citizens must be encouraged to save for their future, because the state must withdraw from providing widespread welfare, restricting it to a bare minimum for genuine need.

- Inheritance taxes and death duties must be rescinded. Families should be allowed to accumulate and pass on wealth which is otherwise destroyed the moment it is acquired by government.

- Protectionist trade policies must be abandoned in favour of free trade. The benefit to an economy from the comparative advantage of buying the best suited products from anywhere are enormous, as the evidence from entrepôt economies, such as Hong Kong, confirms.

- Government ministers must not be permitted to accept lobbying by pressure groups and businesses, because their democratic responsibility is to the entire electorate.

- All central bank activities must cease and replaced by a note issuing authority regulating the relationship between gold coin held in reserve and the face value of notes in circulation. The relationship should be laid down by law, funded by government, and for the gold coin to note relationship to be maintained at a 40% minimum at all times. It must be coin and not bullion in order to be available to the entire population. A bullion standard risks foreign arbitrage in potentially destabilising quantities.

- Foreign policy must be amended to not interfere in other nation’s politics, except where national interests are demonstrably affected.

- Government spending must be fully accountable. All revenue received by the Treasury must be hypothecated — no more robbing Peter to pay Paul.

Clearly, these reforms will not happen before an existential crisis serious enough to force a complete policy overhaul. Even then, it depends on government ministers and bureaucrats correctly diagnosing the reasons for the crisis, which with all of them in thrall to neo-Keynesian macroeconomics and the realisation and admission of their own roles in creating a final crisis is extremely unlikely to happen in a Damascene fashion. Instead, a period of policy vacillation is likely, leading to a danger of political instability and a retreat into yet more socialism.

The final crisis brought upon us by Keynesian policies will almost certainly not mark the end of all our troubles.

Superb.

IMHO the only tax system that will work is one that taxes ‘rents’.

There is only one problem with this. Gold already failed, and is the reason we are in this Fiat mess of ever growing governments and megalomaniac central planners. Gold was good as long as it was directly exchanged to settle transactions: no counterparty risk, no ledger needed to account for anything. Credit has its uses, most notably when the transaction completion depends on a future event that is to happen. Problem is when, as gold is to heavy and slow, and cheaper to custody in a centralized form, it gets replaced by credit in the form of bank notes. Some banks get away, at least sometimes or for some time, with inflating the bank notes in circulation respective to the gold reserves. Authorities see this with envy and get into the game. Whether it was on purpose or not is irrelevant, it was inevitable anyway. Having “infinite money” to “spend at current prices” is so tempting for cantillonaire governments that the gold link had to be broken, sooner or later. Now Fiat is heading to self-destruction, by design, but gold cannot be its replacement, unless some apocalypse takes us back som 300 years or so, where the speed of gold transactions was still acceptable. In fact, we could try gold for some time, but that would require politicians to go against their incentives, will not happen. Most we can expect from them is some kind of gold paper IOUs with varying degrees of trustworthiness, depending on the issuer, not unlike current fiat itself. As Hayek said “I don’t believe we shall ever have a good money again before we take the thing out of the hands of government, that is, we can’t take them violently out of the hands of government, all we can do is by some sly roundabout way introduce something that they can’t stop.” Lets see…