If, in trying to get a grasp of the state of the market for base metals, you were to listen to the likes of Rio Tinto or BHP Billiton, you would be ready to agree with the Neomalthusians that we are barely keeping up with the growing demand for copper – to take but one example – and that, before too long, the urbanization of China will have stripped the planet of every economically extractable ounce of the metal.

Listen to Mark Loveitt—head of the International Wrought Copper Council—however, and you will hear a suggestion that those same rates of demand are already softening markedly as high prices bring about a rapid economisation and a spreading technical substitution of what has become an exceedingly expensive metal for fabricators to employ.

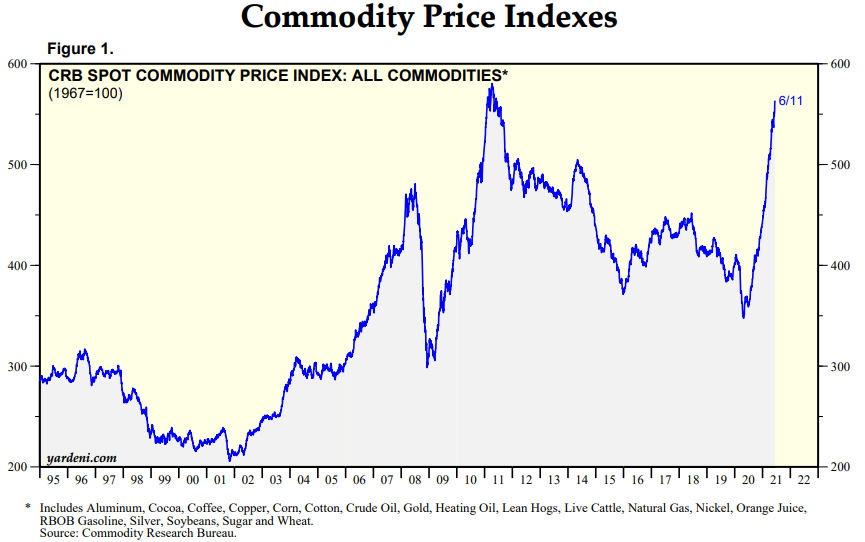

Listen to consulting group Bloomsbury Metals, too, and you will get the impression that we had better make hay while the commodities index fund and ETF sun shines because 2013 onward will see that same mine supply begin to outstrip real end-use just as the rampant investment demand which has helped stimulate that expansion (by boosting prices) itself begins to top out.

Meanwhile, for all the charts so frequently trotted out at shareholder meetings of falling head grades in the world’s ore bodies, Metals Economics Group, for its part, reckons that the top 23 copper miners—responsible for some 70% of global production – managed to replace no less than 290% of their reserves over the boom-time decade to 2010

Yes, widespread delays have once again left the project completions schedules of a few years ago looking hopelessly optimistic – and so have seemingly aggravated the forthcoming supply challenge – but then none of those undertaking such projects managed to foresee the intervening financial crisis either. Hence, after being understandably blind to the degree to which the call upon their services was being artificially inflated, each then contributed to a dramatic, project-delaying slump in investment which was exemplified by a 2-year cumulative reduction of $10 billion in exploration spending from 2008’s all-time peak of $15.6 billion.

That stockpiles of metals mounted skyward as usage fell sharply arguably justified such postponements as occurred, but while the inventory hoards in many cases still persist, a recovery in consumption and the rising prices which have gone with it have meant that any curtailment of capital outlays has also been consigned to the history books by 2011’s imminent, new record level of expenditure.

Nor, while we are on the subject of forecasting, did most of the various official ‘study groups’ who assist in both corporate planning and state policy-making ‘see it coming’, meaning their ideas of the following year’s metals usage—made as late as October 2008 (and, hence, post-LEH) – missed the mark by no less than 11% for zinc and 14% for nickel in 2009!

But forget the cyclical turbulence, implied demand has been and will remain strong, over the long haul, thanks to China’s insatiable appetite – a prediction so largely taken for granted as to be almost axiomatic.

Not so fast, say the likes of Simon Hunt, arguing that all too much of this implied demand (i.e., that calculated backwards from recorded supply and declared stocks) relates not to industrial activity but to financial arbitrage and to a desire to circumvent capital restrictions pertaining to a credit-hungry Middle Kingdom. Nor do the wider mutterings about the on-warrant/off-warrant, delayed load-out games being played at LME warehouses—many now owned by the trading banks, of course—add much comfort that there can be no validity to the ideas of the naysayers.

If, after all, we can now experience sustained periods when metals prices no longer move in the opposite direction to visible stockpiles, or when record inventories coincide with theoretically anomalous cash premia over deferred contracts in the market, we might be forgiven for thinking that not only are the ’fundamentals’ enshrouded in an impenetrable fog of ignorance, but that we no longer even know what is supposed to be ’fundamental’ to what.

After all, the commodity market is not like the equity market in this regard. There, we can study a firm’s balance sheet, pore over its cash flow and income statements, compare its performance to that of both actual and potential competitors and come to some sort of objective estimation about whether it can use its—and, by extension, our — capital wisely and profitably, both now and for the foreseeable range of future circumstances in which we think it must operate.

But when we look at an entity like a grain, or a metal, what can we really say about the ‘fundamentals’ of a whole class of economic goods?

From basic economics, we know that something’s price is supposedly set at the margin when the upper tail of the distribution of buyers ranked by eagerness overlaps numerically with the lower tail of sellers ordered by reluctance and so clears the market—hence why useless, but extremely rare, diamonds command higher prices (in normal circumstances) than vital, but readily available, water.

But that last quantum of expressed ‘eagerness’ is itself a highly subjective entity which should reflect some sort of estimation of that one good’s present and potential, consumptive and productive uses in a whole host of activities of varying degrees of deferability and discretion—some complementary, some competitive, and many highly speculative, not just in the narrow financial usage (though that, too, is obviously of great importance), but also in the wider sense that, at the point of sale, the bid-for material’s value may be nothing more than a twinkle in the bidding entrepreneur’s eye.

Theoretically, this enormous, interacting matrix of actual and possible uses resolves itself into a single number, the price, at the moment of exchange—hence the critical need not to interfere with price formation if scarce goods are to be allocated to their most urgent uses and their value thereby maximised.

An immediate paradox seems to arise here, however, for if the price the most avid man is prepared (and, of course, empowered) to pay is the best—indeed, the only—guide to the worth of the object of his desires, how can we pretend to isolate any other ‘fundamentals’ we might assume to lie behind his choice?

Taking the praxeological approach, we may assume the actions taken to satisfy his needs are rational (if frequently misguided), but we can say nothing about the inner motivation (Mises’ ‘thymology’) which gives rise to those perceived needs.

To take matters to an extreme, we might well value a Tracey Emin daub more for no more than its calorific value as firewood, but we are very likely to be outbid at auction by some well-heeled ‘connoisseur’ conspicuously expressing his elevated sense of aesthetics. Even if we suspect he is no more than a pitiable victim of the intellectually naked-emperorship which comprises much of the modern art movement, we must still allow him his exercise of consumer sovereignty, to the benefit of Ms. Emin’s bank balance (and, effectively, in validation of her artistic entrepreneurship).

In the more mundane case of a buyer or, say, sheet steel (as opposed to soiled sheets!), were we to ask him nicely, we might persuade him to divulge what profit he means to make by his acquisition (a task complicated by the fact that this is not necessarily a pecuniary one) and, if his answer seems unrealistic to us, we might assume his disappointment will translate to a loss and hence to a limitation on both his willingness and ability to repeat his purchase on anything like the same scale in future.

This reckoning might persuade us that the bargain he struck was an anomalous one and that, if we are contending for the same material for our own purposes, we have no need to re-order our individual, subjective schedules as a result of his doings, but that simple perseverance will see our wants fulfilled at an unaltered price. Even here, however, we must also contend with the possibility that his removal of that unit from the available pool (however badly judged in our estimation) may encourage someone else—of whose existence, much less whose motives, or the details of whose prospective cash flow, we may be entirely unaware—to up their tender price instead.

Even assuming our man did take the trouble to explain his reasoning to us and however unconvincing it then seemed, it might just be that he is a better entrepreneur than we, with a better feeling for how the $X he has just laid out on a bolt of cloth, or a billet of chrome alloy, can be parlayed into $X+Y over a suitable period of time.

It should thus be dawning upon us that what we face is a round of infinitely regressing calculus where knowledge of the price paid triggers a burst of entrepreneurial-speculative calculation as to whether existing or planned processes are still worth undertaking if they require this good, the results of which cause further waves of recalculation at one, two, or more removes all along the complex manifold of a productive structure which may wrap several times around the planet before it is done.

Since the functioning market is an adaptive organism which—like its biological equivalents—is powered by disequilibrium gradients (though here composed of prices rather than energy), each change in what Mises liked to call the ‘data’ creates a new economic space in which entrepreneurial arbitrage will again take place but which will simultaneously modify its features and so set off a succession of new bouts of similarly transformative arbitrage.

Sometimes these proceed in a roughly linear and loosely predictable manner, but often in a decidedly non-linear fashion, too. Usually, they are characterised by stabilizing, negative feedbacks – else no calculation and hence no long-duration or divided-labour production would be possible – but occasionally they are wracked by self-reinforcing, positive ones—especially where finance and politics become too closely involved in men’s affairs.

Thus, the price, to some extent, is the most fundamental of all fundamentals, regardless of how that price came to be set—which is not to say that we are unable to recognise when a trajectory of such price changes is becoming dangerously dependent on its own continuation or amplification. This condition often holds sway when the influx of loose money and over-elastic credit which are helping determine that same evolution become confused with capital and when notional gains—foolishly applied to a whole class by a blind extrapolation from each latest, marginal transaction—are conflated with realised ones and so seem to justify the creation of yet more credit with which to extend and quicken the spiral.

Thus, while we may hope to exercise some skill in gauging how well a discrete entrepreneurial unit (the ‘firm’) is navigating these cross-currents in its pursuit of the maximisation of long-term returns to its owners, in the case of many of the things the firm is buying and selling, the definition of ‘fundamentals’ comes down to the tautology that changing prices set in train actions which again change prices. But this restriction does not imply that we must accept the market price as divinely authoritative in the sense which the flawed doctrine of rational expectations or its sub-cult of modern portfolio theory implies.

Nor, to repeat our earlier conviction does this mean that we have no hope of identifying a nascent clustering of errors, or of recognising the building of a constellation of collateral and credit which is sufficiently unstable to be prone to a sudden implosion—i.e., to spot the formation of a ‘bubble’, ahead of it going supernova.

Conversely, nor does it mean that, however solidly the case for one particular investment may seem to be grounded, the aftershocks from the implosions of bubbles grown up in other fields cannot seriously disrupt the premises on which that argument was first built. In Hayek’s words, no entrepreneur can ever really know, alas, his true place in the productive structure and so the Good may be caught up in the ruin of the Bad if not sufficiently buttressed by a sound capital structure.

If we take proper note of the fact that – oh! so many – markets are again merrily up and dancing the Chuck Prince Charleston as if 2008 never happened, we have to accept that, regardless of the seemingly implacable logic of supply, demand, and inventory (none of which are ever quite as concrete as they seem, as we started out by discussing), far too many prices are being set—and far too many entrepreneurial responses to them are being enacted—under the drunk-in-charge misdirection of easy money.

In such a world, what may appear to be ‘fundamental’ may in fact be inconsequential; its use as a yardstick, detrimental; and the risk it will lead to disaster, monumental.

Nice piece.